Introduction: Being debt free with Zero asset.

You’ve just shredded that final debt statement, popped the champagne, and declared yourself financially invincible, debt-free at last! But glance at your balance sheet: zero investments, no property, nada in appreciating assets. Is that victory lap really warranted, or are you missing the bigger picture?

The shocking wealth truth? Debt-free status alone can leave you vulnerable, stagnant, and far from true prosperity. In 2025’s volatile economy, assets, not just absence of debt, are the real game-changers for building net worth and security.

The Shocking Wealth Truth: Debt-Free Myths Exposed

We’ve all heard the cheers for debt-free living, championed by gurus like Dave Ramsey. It’s empowering to escape high-interest traps, but here’s the twist: If you’re debt-free with zero assets, you’re essentially starting from scratch every month.

Net worth, your assets minus liabilities, tells the full story. Zero debt means zero liabilities, but without assets like stocks or real estate, your net worth flatlines at zero. As a Forbes article warns, rushing to debt-free can overlook opportunities, like using low-interest loans for income-generating assets.

This mindset shift is crucial in 2025, where inflation erodes cash and AI disrupts jobs. Being debt-free feels safe, but without assets, you’re one emergency away from borrowing again.

Why Zero Assets Undermine Your Debt-Free Win

Imagine two people: Alex, debt-free with $10K in savings, and Jordan, with $50K debt but $200K in rental properties netting $2K monthly. Who’s wealthier? Jordan’s positive cash flow builds equity over time.

The shocking wealth truth is assets create wealth multipliers, appreciation, income, tax perks. Zero assets? You’re reliant on earned income alone, which caps your growth. A Rich Dad post emphasizes: Good debt acquires assets; bad debt buys liabilities.

In 2025, with home prices up 5% yearly per recent trends, skipping asset-building means missing compounding magic. Debt-free is a milestone, not the endgame.

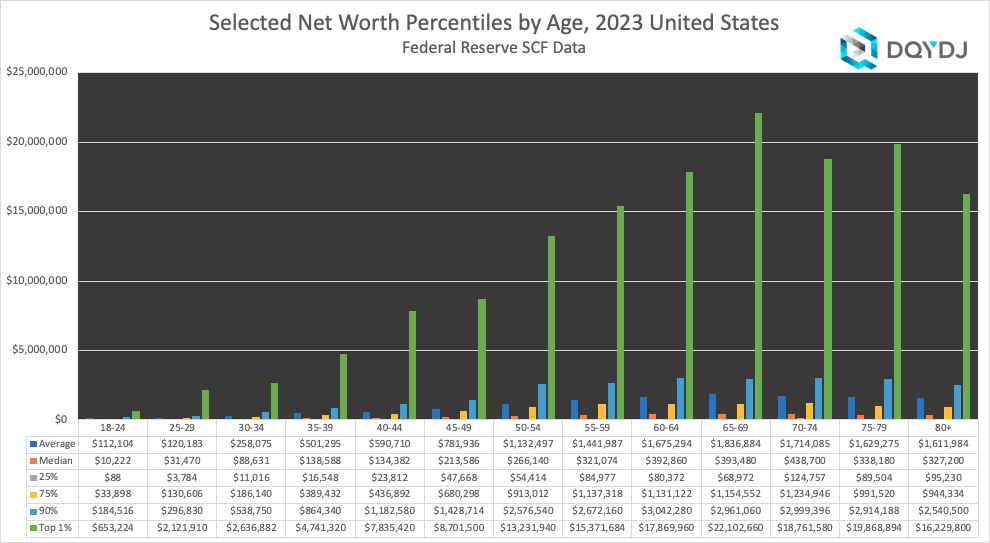

Net Worth Basics: The Shocking Wealth Truth in Numbers

Net worth isn’t jargon, it’s your financial scorecard. Assets (what you own: cash, investments, property) minus liabilities (debts) equals net worth.

Why care? High net worth means freedom, retire early, weather storms. But 2025 stats reveal a shocking divide: Many debt-free folks hover at low net worth due to asset neglect.

From the Federal Reserve’s latest data, medians lag, but top earners boast assets driving growth. Ignoring this truth? You’re playing defense only.

2025 Net Worth Stats: Where Do You Stand Without Assets?

Let’s crunch numbers. 2025 updates show stark realities, debt-free but asset-poor keeps you median or below.

Here’s a table comparing average vs. median net worth by age, highlighting asset impact (data from Fidelity and Kiplinger):

| Age Group | Median Net Worth | Average Net Worth | Top 25% Net Worth | Key Asset Driver |

|---|---|---|---|---|

| Under 35 | $39,000 | $183,000 | $100,000+ | Early investments |

| 35-44 | $135,000 | $548,000 | $350,000+ | Home equity & stocks |

| 45-54 | $247,000 | $971,000 | $700,000+ | Retirement accounts |

| 55-64 | $364,000 | $1,564,000 | $1,000,000+ | Diversified portfolios |

| 65-74 | $410,000 | $1,200,000+ | $1,200,000+ | Income-generating assets |

| 75+ | $335,000 | $900,000+ | $900,000+ | Legacy investments |

Shocking, right? Averages skew high due to asset-rich outliers. Without assets, even debt-free folks cluster at medians, missing wealth acceleration.

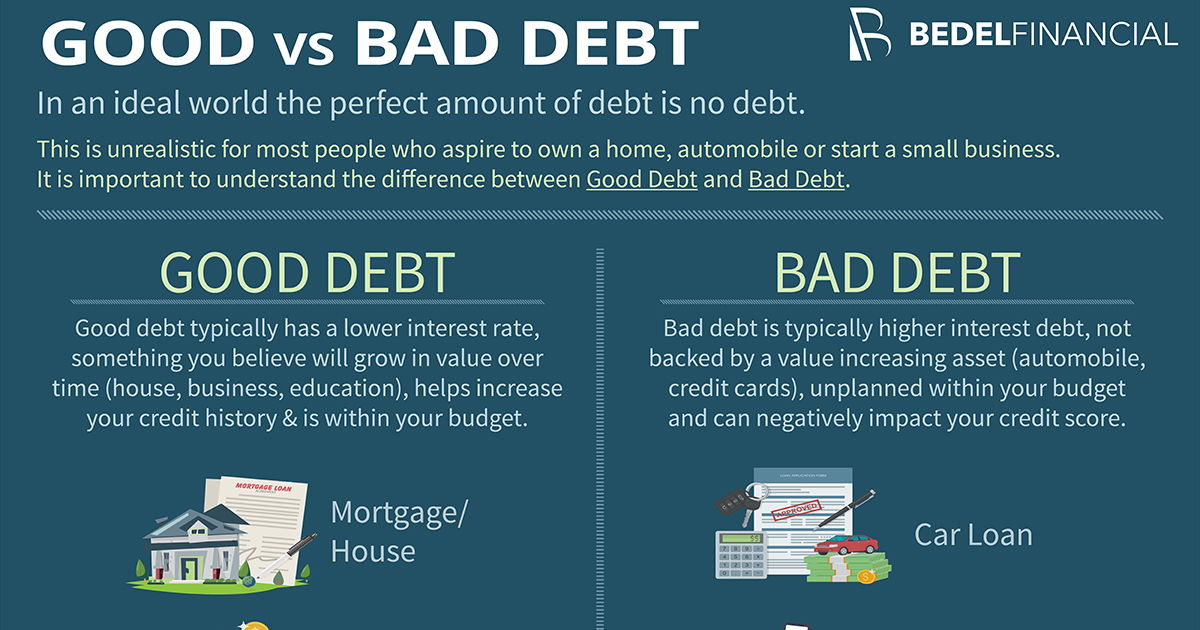

Good Debt vs. Bad Debt: The Shocking Wealth Truth Revealed

Not all debt is evil, here’s the revelation: Good debt builds assets; bad debt drains them.

Bad debt? High-interest credit cards for consumables, think 20% APR on gadgets that depreciate. It erodes net worth fast.

Good debt? Low-rate mortgages or business loans for appreciating assets. As I Will Teach You to Be Rich explains, it leverages money to multiply wealth.

In 2025, with rates stabilizing, good debt like student loans for high-ROI careers or real estate financing can outpace inflation. The truth: Debt-free zealots often shun this, staying asset-poor.

Leveraging Good Debt: Build Assets Without Going Broke

Ready for action? Use good debt strategically.

- Mortgages: Buy property with 3-4% rates; rents cover payments, equity grows. Per Rich Dad, it’s OPM (other people’s money) at work.

- Student Loans: For degrees boosting income 20-50%, per labor stats.

- Business Loans: Start ventures; deduct interest, scale profits.

Key: Debt-to-income under 36%, as Schwab advises. This flips debt-free scripts—assets first, then payoff.

Real Stories: From Debt-Free to Asset-Rich Transformations

Take Sarah, 38, who went debt-free by 35 but had $0 assets. “I felt stuck,” she shares in a Reddit thread. She took a low-rate loan for a duplex, now nets $1,200/month, net worth $150K+.

Or Mike, inspired by White Coat Investor: Paid bad debt, used good for investments. From zero to $500K in five years.

These aren’t rarities—Bankrate stories show asset focus post-debt-free sparks true freedom.

Common Pitfalls: Why Debt-Free Folks Stay Asset-Poor

Many hit debt-free then coast, big mistake.

- Fear of Debt Return: Trauma blocks good debt opportunities.

- No Investment Education: Schools skip this; result? Cash hoarding.

- Lifestyle Creep: Extra cash spent, not invested.

- Ignoring Inflation: Cash loses 3-5% value yearly in 2025.

As Kingsview warns, debt-free ≠ financially free. Overcome by educating via books like “Rich Dad Poor Dad.”

Steps to Build Assets Post-Debt-Free

Transition smoothly:

- Emergency Fund First: 3-6 months expenses in high-yield savings.

- Invest Basics: Start with index funds; Schwab’s guide helps.

- Explore Good Debt: Pre-qualify for asset loans.

- Diversify: Mix stocks, real estate, side hustles.

- Track Net Worth: Monthly reviews via apps.

- Seek Advice: Free tools from Experian.

Aim for 15-20% income to assets yearly. In 2025, robo-advisors make it easy.

2025 Trends: Assets in a Changing Economy

With AI boosting productivity and crypto maturing, assets evolve. Sustainable investing grows 15% yearly, per McKinsey.

Debt-free purists miss this, focus on ESG funds or real estate tech. The shocking truth: Adapt or lag.

Balancing Act: Debt-Free and Asset-Building Harmony

You don’t choose one, blend them. Pay bad debt aggressively, use good for assets.

Result? Positive net worth trajectory. As New York Life notes, this builds quality life without regret.

The Long-Term View: Shocking Wealth Truth for Retirement

Fast-forward: Debt-free at 65 with zero assets? Social Security alone, per Visual Capitalist. Asset-rich? Passive income funds dreams.

2025 BCG report: Net new assets drive firm values, same for personal wealth.

Wrapping the Shocking Wealth Truth

We’ve unpacked the shocking wealth truth: Debt-free shines, but zero assets dims it. From stats to strategies, assets are your wealth engine.

Don’t flex debt-free alone, build that portfolio. In 2025, it’s your edge.

CTA: Ready to asset-up? Check Rule One Investing’s guide for starters. Share if this revelation hit home. What’s your first asset move? Comment! Read more on good debt at Michigan First. Share now!