Introduction: Life-Changing Income Decisions Before 30

The decisions you make about your income in your 20s feel small at the time, another coffee run, skipping a 401(k) contribution, or passing on a salary negotiation. But compound them over decades, and they quietly decide whether you retire comfortably or worry about bills forever.

These income decisions before 30 aren’t flashy. They’re everyday choices that harness time, your greatest asset. Get them right, and wealth builds almost effortlessly. Get them wrong, and catching up becomes exponentially harder. In 2026, with rising costs and shifting job markets, these 9 income decisions before 30 are more powerful than ever.

Why Income Decisions Before 30 Matter So Much for Building Wealth

Your 20s offer unmatched leverage: time for compound growth, fewer responsibilities, and maximum earning potential ahead. According to financial experts, starting smart habits early can multiply wealth exponentially.

For instance, Investopedia highlights that young adults who invest early benefit from compound interest as their “superpower.” Small amounts grow dramatically over decades. Delay, and you miss out on hundreds of thousands.

These income decisions before 30, how you earn, allocate, and grow your money, set the trajectory. Let’s dive into the nine that separate those who build wealth from those who struggle.

Income Decision 1 Before 30: Starting to Invest a Portion of Your Income Early

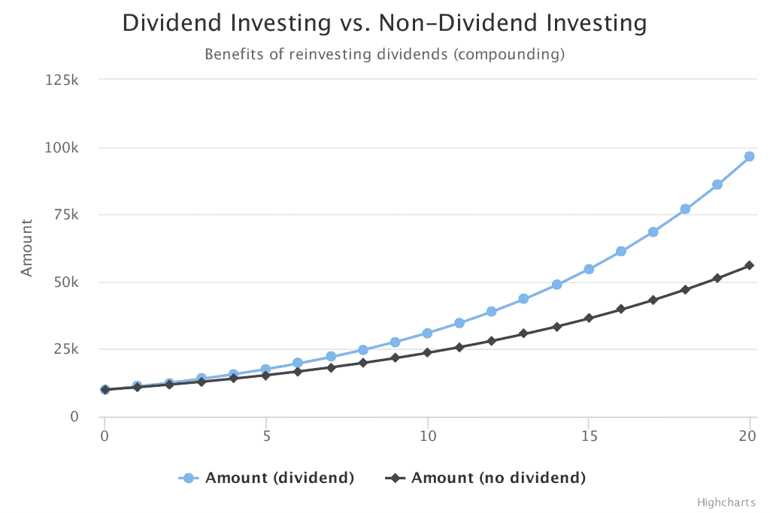

One of the most powerful income decisions before 30 is committing to invest regularly, even modestly. Open a Roth IRA or contribute to a 401(k), especially if your employer matches.

Why it matters: Compound interest turns small contributions into massive sums. Investing $200 monthly at 7% return from age 25 to 65 yields about $525,000. Start at 35? Only $244,000, a $281,000 difference.

As Fulton Bank advises, automate contributions to capture employer matches, free money that boosts wealth.

This income decision before 30 prioritizes future you over instant gratification.

Income Decision 2 Before 30: Building and Monitoring Your Credit Score

Your credit score influences borrowing costs for homes, cars, and even jobs. One of the smartest income decisions before 30 is treating credit responsibly: pay on time, keep utilization low, and monitor regularly.

Good credit saves thousands in interest. Poor credit locks you into higher rates, draining income.

Wisely by ADP recommends checking your score annually and using tools to build it steadily. This decision protects your income from unnecessary expenses.

Income Decision 3 Before 30: Avoiding or Aggressively Paying High-Interest Debt

High-interest debt (credit cards, payday loans) is wealth’s enemy. Choosing to avoid unnecessary debt or pay it off fast is a critical income decision before 30.

Interest compounds against you. A $5,000 credit card balance at 20% interest costs far more than the principal if only minimums are paid.

Experts suggest the debt avalanche or snowball method. Fulton Bank notes redirecting funds to debt frees income for investing.

This income decision before 30 prevents debt from stealing future wealth.

Income Decision 4 Before 30: Adopting a Smart Budgeting System Like 50/30/20

How you allocate income defines wealth. Using the 50/30/20 rule, 50% needs, 30% wants, 20% savings, is a game-changing income decision before 30.

It ensures balance while forcing savings. Wisely by ADP explains this rule builds habits that prevent lifestyle creep.

Track spending monthly. This decision keeps more income working for you.

Income Decision 5 Before 30: Automating Your Savings and Investments

Automation removes temptation. Setting up automatic transfers for savings, investments, and retirement is a quiet but powerful income decision before 30.

Wisely by ADP suggests splitting direct deposits. This “pay yourself first” habit builds wealth effortlessly.

Consistency trumps motivation every time.

Income Decision 6 Before 30: Building a Solid Emergency Fund

An emergency fund covers 3-6 months of expenses. Building one early protects income from setbacks like job loss or repairs.

Without it, you might rely on debt. Investopedia stresses this cushion provides security to pursue opportunities.

This income decision before 30 safeguards your progress.

Income Decision 7 Before 30: Investing in Career Growth and Salary Negotiation

Your income potential skyrockets with deliberate career moves. Negotiating salaries, seeking promotions, or switching jobs for higher pay is an essential income decision before 30.

Forbes notes job switches often yield 9-10% raises. Investing in skills increases earning power long-term.

This decision amplifies all other income decisions.

Income Decision 8 Before 30: Starting Side Hustles or Multiple Income Streams

Relying on one income source is risky. Launching a side hustle, freelancing, online business, or investments, diversifies and accelerates wealth.

Extra income funds investments faster. Many build significant wealth this way in their 20s.

This income decision before 30 creates resilience and opportunity.

Income Decision 9 Before 30: Continuously Upskilling for Higher Earning Potential

The world changes fast. Investing in education, certifications, or skills that boost income is a forward-thinking income decision before 30.

Higher skills mean higher paychecks. Savvy Wealth emphasizes lifelong learning as key to financial confidence.

This decision ensures your income grows with time.

Comparing the Impact: A Quick Table on These Income Decisions Before 30

To visualize the power, here’s a table showing approximate long-term effects (based on average scenarios):

| Income Decision Before 30 | Short-Term Effort | Long-Term Wealth Impact (to Age 65) | Example Benefit |

|---|---|---|---|

| Invest Early | Medium | +$500K+ from compounding | $200/month → $525K |

| Build Credit | Low | Thousands saved on interest | Lower loan rates |

| Pay Off High-Interest Debt | High | Debt-free freedom | Avoid 20%+ interest traps |

| Adopt 50/30/20 Budget | Medium | Consistent savings growth | 20% of income invested |

| Automate Savings | Low | Effortless wealth accumulation | “Set it and forget it” |

| Build Emergency Fund | Medium | Protection from setbacks | No forced debt |

| Career Growth & Negotiation | Medium-High | 10-50% higher lifetime earnings | Job switches boost pay |

| Start Side Hustles | High | Diversified income streams | Extra $1K+/month |

| Continuous Upskilling | Medium | Ongoing income increases | Higher salary trajectory |

These income decisions before 30 compound, combine them for exponential results.

Putting It All Together: Your Action Plan for These Income Decisions Before 30

Start small but start now. Pick 2-3 decisions and implement:

- Automate a small investment contribution.

- Review your budget this week.

- Negotiate your next raise or update your resume.

Track progress quarterly. Adjust as life evolves. In 2026, tools like apps and online courses make these easier than ever.

The beauty? These income decisions before 30 reward consistency over perfection.

Final Thoughts: Make These Income Decisions Before 30 and Watch Wealth Follow

Your 20s aren’t for “figuring it out later”, they’re for setting the foundation. These 9 life-changing income decisions before 30 quietly build the wealth most people only dream of.

You don’t need a high salary to start. You need intentional choices. Which of these income decisions before 30 will you tackle first?

CTA: Take action today, calculate your compound growth with a free tool or download a budgeting template. Share this post with a friend in their 20s. Comment your top priority below! Read more on early investing? Check Investopedia. Share now!