Introduction: Wealth Destruction.

Ever stared at your bank statement, wondering where all that hard-earned cash vanished? It’s not magic, it’s math, sneaky and relentless, chipping away at your wealth while you sleep.

In 2026, with inflation lingering and markets volatile, these hidden forces are more potent than ever. But here’s the twist: Property owners aren’t losing sleep. They’re leveraging real estate to counter these destroyers, building buffers that let them rest easy.

Unmasking the Hidden Math Behind Wealth Destruction in 2026

Wealth doesn’t evaporate overnight, it’s a slow burn driven by mathematical realities most ignore until it’s too late. Drawing from recent economic analyses, these factors compound, turning modest savings into dust.

Think of it like a leaky bucket. You pour in earnings, but unseen holes drain it faster than you fill. In 2026’s economy, understanding this math isn’t optional, it’s survival.

Let’s break down the five shocking culprits, backed by data and expert insights.

Hidden Math 1: Inflation’s Compound Erosion, The Silent Wealth Killer

Inflation isn’t just higher prices, it’s a mathematical thief eroding your purchasing power exponentially. At 3% annual inflation, your $100 today buys only $74 in 10 years.

This compounds: Over 30 years, that same dollar shrinks to $41. Shocking? Absolutely. As Moran Wealth Management explains, it reshapes goals—retirement savings must grow faster just to stand still.

- Daily Impact: Groceries up 5%? That’s wealth destruction in your cart.

- Long-Term Toll: Fixed incomes lag, widening gaps.

Property owners? They hedge this with appreciating assets.

Hidden Math 2: Tax Drag, How Uncle Sam Multiplies Your Losses

Taxes aren’t flat, they drag on returns, compounding losses over time. A 25% tax on 8% gains nets just 6%, halving wealth growth in decade.

In 2026, with potential policy shifts, this math bites harder. Russell Investments’ graphs illustrate how deferred taxes preserve compounding.

- Capital Gains Trap: Sell assets? Lose 15-20% instantly.

- Income Bracket Creep: Inflation pushes you higher without real gains.

Real estate counters with deductions, letting owners sleep sound.

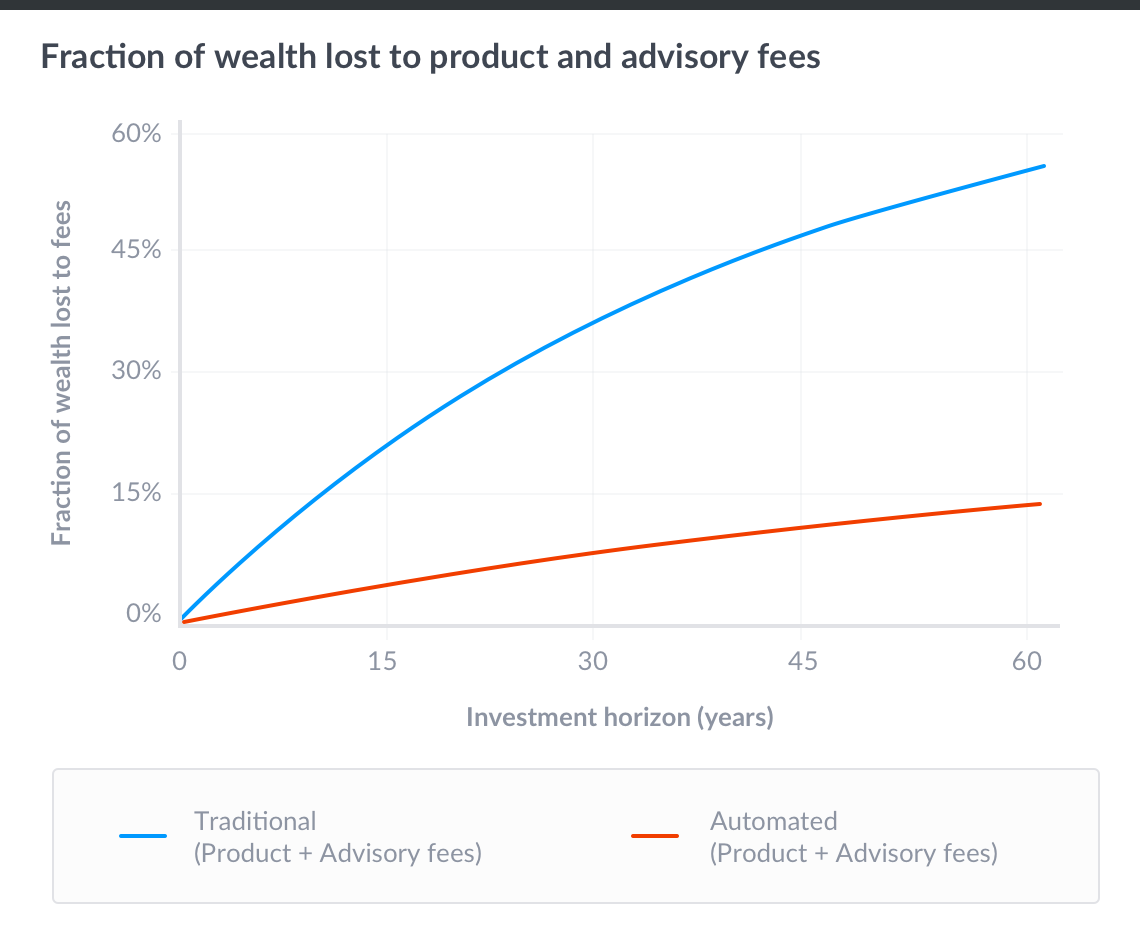

Hidden Math 3: Compound Fees, The Invisible Wealth Eater

Fees seem tiny, 1% annually? Harmless. But compounded, they devour. A $100K portfolio at 7% return minus 1% fees grows to $574K in 30 years vs. $761K fee-free.

This “tyranny of compounding costs” erodes 25%+ of potential wealth. In 2026’s fee-heavy funds, it’s a silent destroyer.

- Mutual Fund Pitfall: Average 0.5-2% eats returns.

- Advisor Fees: Add 1%? Double the damage.

Property? Low ongoing costs, high control.

Hidden Math 4: Opportunity Cost, The Price of Playing It Safe

Holding cash? Safe, right? Wrong. Opportunity cost is the math of what you miss. At 2% inflation, $100K in a 1% savings account loses $1K yearly in real terms.

In 2026, with rates fluctuating, idle cash misses stock or real estate gains averaging 7-10%. Over 10 years, that’s $100K forgone.

- Cash Hoarding Risk: Feels secure, but erodes wealth.

- Delayed Investing: Wait for “perfect” time? Lose compounding.

Real estate flips this, leverage amplifies returns.

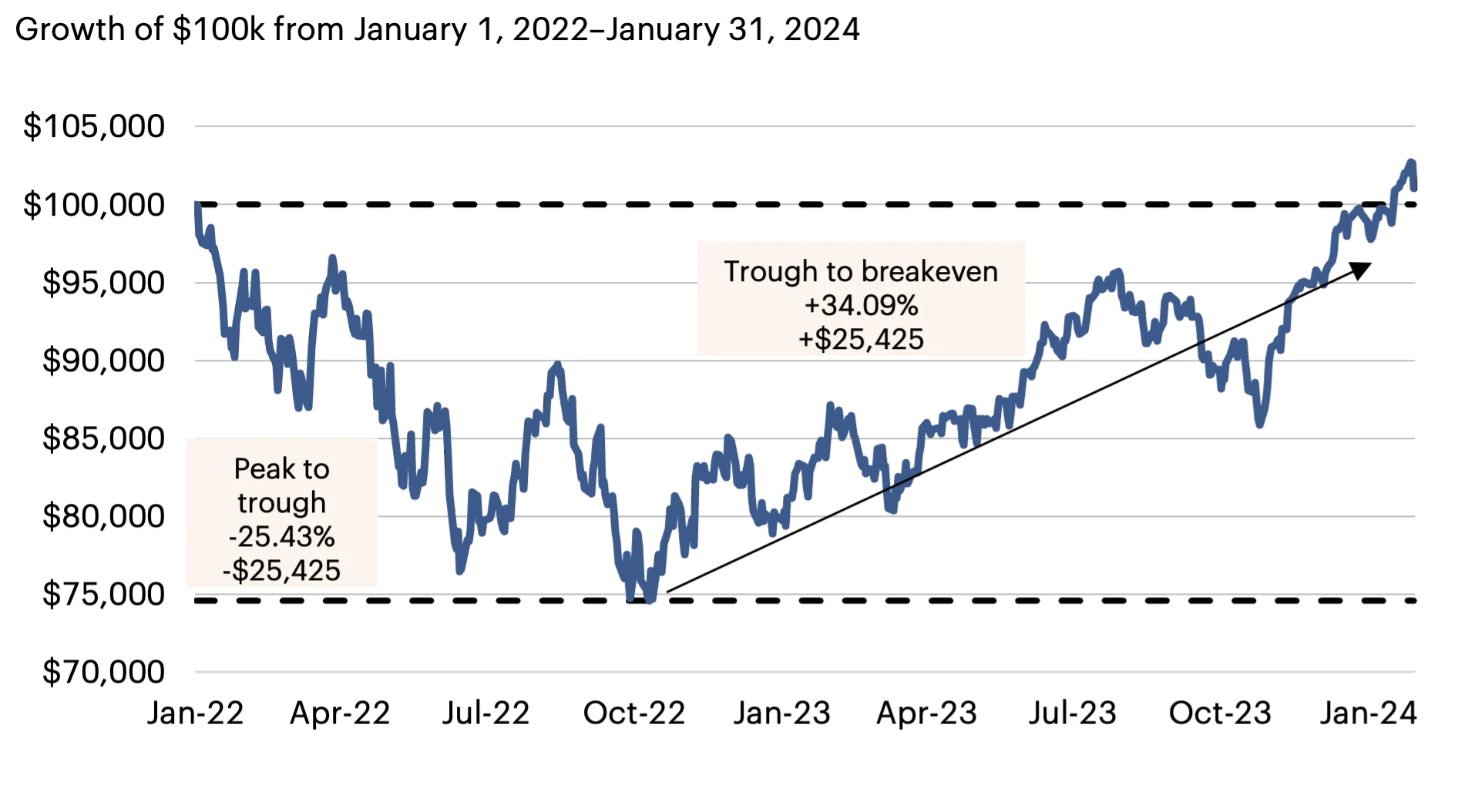

Hidden Math #5: Asymmetric Recovery, Why Losses Hurt More Than Gains Help

Drop 50%? Need 100% gain to recover. This asymmetry destroys wealth in volatile markets. A $100K portfolio falling to $50K requires doubling to break even.

In 2026’s uncertain economy, one dip wipes years of progress. Springer research shows risk transmission amplifies this.

- Volatility Trap: Gains linear, losses exponential.

- Behavioral Bias: Panic sells lock in destruction.

Property’s stability minimizes these swings.

Comparing the Hidden Math: Wealth Destruction vs. Real Estate Protection

To visualize, here’s a table contrasting these destroyers with real estate’s counters, inspired by World Inequality Lab data.

| Hidden Math Destroyer | Mathematical Impact | Real Estate Hedge | Why It Works |

|---|---|---|---|

| Inflation Erosion | Compounds loss at 3-5%/year | Appreciation & Rent Adjustments | Values rise 4-5%/year; rents track inflation Primior |

| Tax Drag | Reduces net returns 20-30% | Deductions & Depreciation | Offset income; 1031 exchanges defer gains Yahoo Finance |

| Compound Fees | Eats 25%+ of growth | Low Management Costs | Direct ownership minimizes fees Wealthfront |

| Opportunity Cost | Forgone 7-10% returns | Leverage & Equity Build | Borrow at 4-6%; gain 10%+ appreciation Financial Symmetry |

| Asymmetric Recovery | 50% loss needs 100% gain | Tangible Stability | Low volatility; holds value in crashes Digonzini |

This math shows real estate isn’t just an asset, it’s armor.

Why Property Owners Sleep Better: Real Estate’s Math-Busting Power

Now, the good news. Property owners sleep better because real estate flips destruction math into creation. As Financial Samurai notes, it’s a multi-hedge.

First, against inflation: Properties appreciate, rents rise. CrowdStreet research shows CRE outperforms during high inflation.

Real Estate Advantage 1: Leverage, Multiply Wealth with Borrowed Math

Borrow 80% at 5%, property up 7%? Your 20% equity gains 35%. This good debt amplifies returns, per All Property Management.

- Risk Managed: Fixed rates lock costs.

- Equity Snowball: Tenants pay down principal.

In 2026, low rates make this golden.

Real Estate Advantage 2: Tax Shields, Turn Destruction into Deductions

Depreciation, mortgage interest, 1031 exchanges, real estate’s tax math saves thousands. GOBankingRates highlights how wealthy use this to build empires.

- Depreciation Magic: Write off “wear” without cash outlay.

- Capital Gains Deferral: Roll profits tax-free.

Sleep better knowing taxes work for you.

Real Estate Advantage 3: Passive Income, Compound Creation Over Destruction

Rents provide steady cash flow, covering costs and more. Bob Lucido Team notes this builds wealth hands-off.

- Inflation-Proof: Adjust rents yearly.

- Diversification: Low stock correlation.

In volatile 2026, this stability shines.

Real Estate Advantage 4: Appreciation, The Anti-Erosion Force

Homes gain 4-5% yearly historically. Forced appreciation via upgrades boosts this, as Excelsior Capital details.

- Market Forces: Demand drives values.

- Long-Term Win: Outpaces inflation consistently.

Property owners watch wealth grow while sleeping.

Real Estate Advantage 5: Tangible Security, Hedge Against Asymmetry

Unlike stocks, real estate doesn’t vanish. It provides utility and low volatility.

- Crash Resilience: Holds value; generates income.

- Diversification Power: Balances portfolios.

In 2026’s uncertainties, this lets owners rest easy.

Overcoming Real Estate Myths: Why It’s Accessible in 2026

Think property’s too risky? Math says otherwise. With low barriers via REITs or crowdfunding, anyone starts small. Real Estate Skills guides beginners to success.

- Start Small: Buy rental with 20% down.

- Mitigate Risks: Insurance, due diligence.

Rewards outweigh hidden destructions.

Building Your 2026 Strategy: Counter Wealth Destruction with Property

Ready to flip the script? Assess your exposure to these math destroyers. Then, explore real estate, consult advisors, crunch numbers.

- Step 1: Calculate inflation impact on savings.

- Step 2: Review tax/fee drags.

- Step 3: Explore property options.

As Kiplinger affirms, it’s supreme for wealth preservation.

Conclusion: Don’t Let Hidden Math Destroy Your Wealth, Join the Property Owners Who Sleep Soundly

We’ve exposed the shocking five hidden math behind wealth destruction, from inflation’s creep to asymmetry’s bite. Yet, property owners sleep better, armed with hedges that turn math in their favor.

In 2026, ignore this at your peril. Embrace real estate’s power for security and growth. Your peaceful nights await.

CTA: Ready to shield your wealth? Explore Top Team Homes’ 2026 market insights. Share this if it woke you up. What’s your biggest wealth worry? Comment below! Read more on hedges at Vaster Blog. Share now!