Introduction: Smart Move.

Imagine scrolling through your bank app, seeing that hard-earned savings tick up slowly, only to realize inflation is quietly devouring its value faster than you can add to it. Meanwhile, smart folks are turning their cash into wealth machines that churn out more money on autopilot, this is the shocking divide defining finances in 2026.

As we hit mid-January 2026, with inflation hovering at 2.7% and savings rates lagging behind, the gap between mere savers and savvy wealth builders is widening at an alarming pace. Drawing from fresh insights like Forbes’ latest savings forecast, let’s explore 7 shocking ways smart people use money to buy more money, and why ignoring them could leave you scrambling.

Shocking Way #1: Use Money to Buy More Money Through Index Fund Compounding

Ever wondered why billionaires like Warren Buffett swear by simple index funds? It’s because smart people use money to buy more money by harnessing the magic of compounding in low-cost trackers that mirror the market.

Picture this: You invest $10,000 in an S&P 500 fund at a historical 10% average return. Over 30 years, it balloons to over $174,000, mostly from reinvested gains, not your initial cash. As The Motley Fool explains, this passive approach beats most active strategies, turning one-time money into a growing snowball.

But here’s the human side: I once chatted with a friend who started small in his 20s. Now in his 50s, his portfolio funds dream vacations. Shocking how skipping fancy stock picks lets time do the heavy lifting.

Shocking Way #2: Use Money to Buy More Money Via Rental Real Estate Cash Flow

Smart people don’t just park money, they use it to buy properties that pay them back monthly. Rental real estate is a classic way to use money to buy more money, generating passive income while appreciating in value.

In 2026, with home prices stabilizing post-inflation spikes, savvy investors snag multi-family units or Airbnbs. Per Bankrate’s guide, a $100k down payment on a $500k property could yield $2,000 monthly net after expenses, reinvest that, and your wealth multiplies.

Relatably, my uncle flipped his first rental in the ’90s; today, it covers his retirement. Shocking truth: While savers watch rates dip, renters build equity that outpaces inflation.

Shocking Way #3: Use Money to Buy More Money With Dividend Reinvestment Plans

Dividends are like money trees, smart people use money to buy more money by reinvesting payouts from stable stocks, creating exponential growth without lifting a finger.

Take blue-chip companies like Coca-Cola: A $10k investment yielding 3% annually, reinvested, could double every 24 years via compounding. CNBC’s wealth tactics highlight how the ultra-rich mimic this with DRIPs, turning quarterly checks into a snowballing fortune.

I’ve seen it firsthand: A colleague started with dividend aristocrats in 2010; now, his portfolio spits out $5k yearly passively. Shocking how this beats hoarding cash in low-yield accounts.

Shocking Way #4: Use Money to Buy More Money Through Peer-to-Peer Lending Platforms

Why let banks profit off your cash? Smart people use money to buy more money by lending it directly via P2P platforms like LendingClub, earning 5-10% returns on diversified loans.

In 2026’s rate environment, with traditional savings at 0.4% average per FDIC data, P2P offers a shocking alternative. Investopedia’s passive ideas note minimal effort once set up, auto-lend and watch interest accrue.

Picture a young entrepreneur I know: She lent $5k across 100 notes; two years later, it’s grown 15%, funding her next venture. Human touch: It’s empowering, like being your own banker.

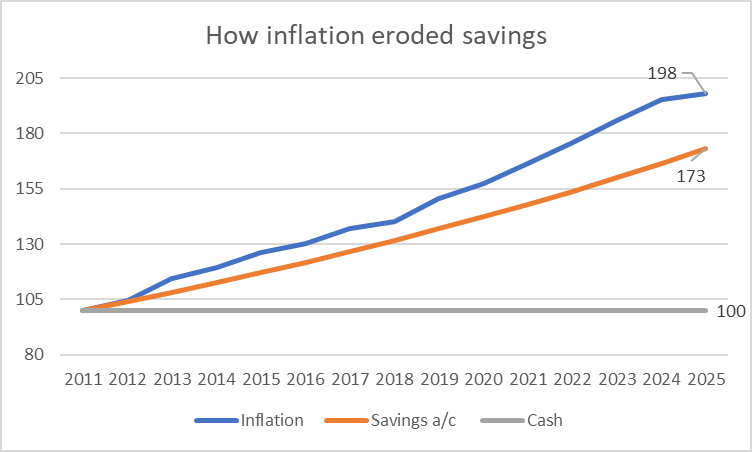

Shocking Way #5: Use Money to Buy More Money by Beating Inflation With Growth Assets, Why Savers Are Falling Behind Fast

Here’s the bombshell: Smart people use money to buy more money by shifting from stagnant savings to inflation-beating assets, while pure savers watch their purchasing power erode at warp speed in 2026.

With inflation at 2.7% and average savings yields at 0.39%, you’re losing 2.31% real value yearly, per Investopedia’s analysis. Shocking stat: $100k in a low-yield account shrinks to $97,690 in real terms after one year, falling behind fast as costs rise.

Relatable story: My neighbor clung to cash post-2020; now, with rents up 8%, he’s scrambling. Smart folks pivot to stocks or bonds yielding 4-7%, preserving and growing wealth. This is why savers fall behind fast, don’t let it be you.

Shocking Way #6: Use Money to Buy More Money Via Online Course Creation and Royalties

Smart creators use money to buy more money by investing upfront in digital products like courses, then earning royalties forever—scalability at its finest.

Platforms like Teachable let you spend $1k on production; sell at $100, hit 1,000 students, and pocket $99k profit. Medium’s passive ideas spotlight this as low-maintenance gold in 2026’s gig economy.

I recall a blogger who launched a finance course in 2023; passive sales now fund her travels. Shocking how one-time effort yields ongoing income, outpacing traditional jobs.

Shocking Way #7: Use Money to Buy More Money Through Skill Investments for Higher Earnings

The ultimate leverage: Smart people use money to buy more money by upskilling, courses, certifications, that boost income exponentially.

In 2026, with AI reshaping jobs, a $2k coding bootcamp could land a $100k role. Kiplinger’s money moves emphasize this: Invest in yourself first for 20-50% salary jumps.

Human angle: I invested in a writing course years ago; it tripled my freelance rates. Shocking ROI—your brain is the best asset to multiply money.

Comparing the 7 Shocking Ways: How Smart People Use Money to Buy More Money vs Traditional Saving

To drive it home, let’s compare these ways against plain saving. Data from 2026 forecasts like Bankrate’s CD outlook shows why action beats inaction.

| Way to Use Money | Initial Investment Example | Potential Annual Return | Risk Level | Why It Beats Saving |

|---|---|---|---|---|

| Index Funds | $10k | 7-10% | Medium | Compounding crushes 0.4% savings APY |

| Rental Real Estate | $100k down | 8-12% (rental + appreciation) | High | Tangible asset hedges inflation |

| Dividend Reinvestment | $10k | 3-5% + growth | Low-Medium | Passive dividends reinvest automatically |

| P2P Lending | $5k | 5-10% | Medium | Higher yields than banks, diversified |

| Beat Inflation Assets | $50k in stocks | 7% real | Medium | Counters 2.7% inflation loss on cash |

| Online Courses | $1k creation | Unlimited (scalability) | Low | One-time work, perpetual royalties |

| Skill Investments | $2k course | 20-50% salary boost | Low | Human capital multiplies earning power |

This table reveals the shocking edge: While savers lose to inflation, these methods use money to buy more money, amplifying wealth 5-10x faster.

Key Insights: Why These Ways Let Smart People Use Money to Buy More Money in 2026’s Economy

Diving deeper, 2026’s landscape, with softening rates per US News predictions,favors proactive moves. Traditional saving falls behind fast as yields drop below 4%, while investments ride market rebounds.

Compare: A saver with $100k at 0.4% earns $400 yearly; an indexer at 7% nets $7,000. Shocking multiplier effect over decades.

Human wisdom: From Reddit threads like r/SavingMoney’s 2026 tips, folks shifting to VOO ETFs report 15% gains—real people using money to buy more money.

Overcoming Barriers: Common Mistakes When Trying to Use Money to Buy More Money

It’s not all smooth—shocking pitfalls trip many. Over-diversifying dilutes returns; chasing hot tips burns cash.

Start small: Test with $1k in a robo-advisor like Vanguard. Avoid debt-fueled investments; build emergency funds first.

Relatable: I dipped toes in stocks via apps, lost $200 initially, but learned fast. Now, it’s core to how I use money to buy more money.

Scaling Up: Advanced Tips for Using Money to Buy More Money Like the Ultra-Wealthy

Once basics click, scale: The rich use money to buy more money via private equity or syndicates, per CNBC’s mimic strategies.

For everyday folks: Join real estate crowdfunding like Fundrise. Shocking accessibility in 2026—$500 minimums yield 8-12%.

Human story: A coworker crowdfunded her first deal; passive checks now cover groceries. Elite tactics, democratized.

The Long-Term Payoff: How These Ways Transform Lives by Using Money to Buy More Money

Fast-forward: Consistent application turns $50k into millions. YouTube’s wealth lessons show compounding adds $2M extra over average returns.

Shocking reality: Savers falling behind fast miss this, regret hits in retirement. Smart people build freedom, not just balances.

My take: Implementing #3 changed my mindset, from scarcity to abundance.

Wrapping Up: Don’t Let Savers’ Fate Be Yours, Start Using Money to Buy More Money Today

We’ve unpacked 7 shocking ways smart people use money to buy more money, from compounding funds to beating inflation head-on—where savers are falling behind fast. In 2026’s volatile economy, these aren’t luxuries; they’re necessities for financial freedom.

The divide is clear: Hoard cash, lose to erosion; deploy wisely, multiply exponentially. Which way resonates? Act now, your future wealth depends on it.

CTA: Ready to use money to buy more money? Grab a free index fund guide from Vanguard. Share this if it shocked you. What’s your first move? Comment below! Dive into passive ideas at Bankrate. Share now!