Introduction: HSBC Cut Rate Consequences.

Imagine scrolling through your morning news feed in early January 2026, spotting headlines about HSBC slashing mortgage rates, the first big lender to do so this year. You think, “Finally, a break for homebuyers!” But what if this move signals deeper economic troubles that end up dragging UK property prices lower instead of lifting them?

That’s the shocking twist we’re unpacking today. While lower rates typically boost affordability and spark demand, in a fragile economy like ours right now, they could unleash a chain reaction pushing prices down. Drawing from fresh data and expert insights, let’s dive into why HSBC’s cut might not be the property party we hoped for.

HSBC’s Rate Cut: The Shocking Spark for UK Property Prices 2026 Volatility

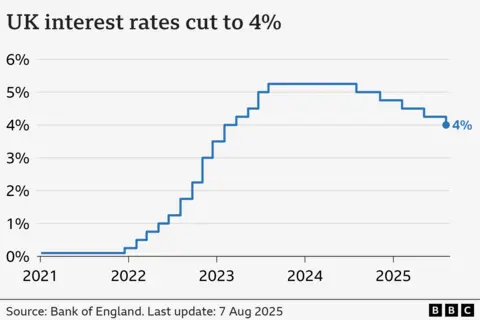

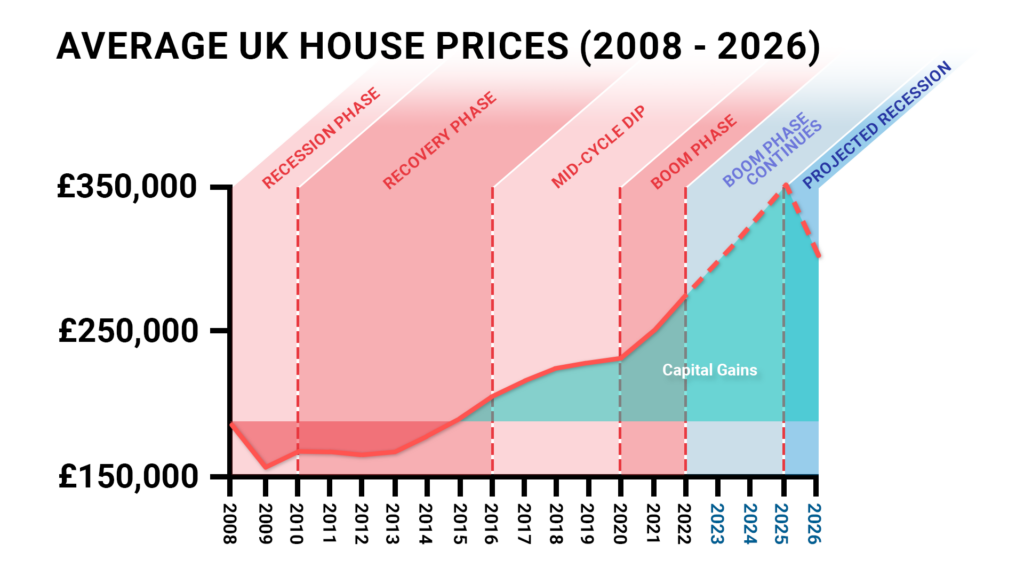

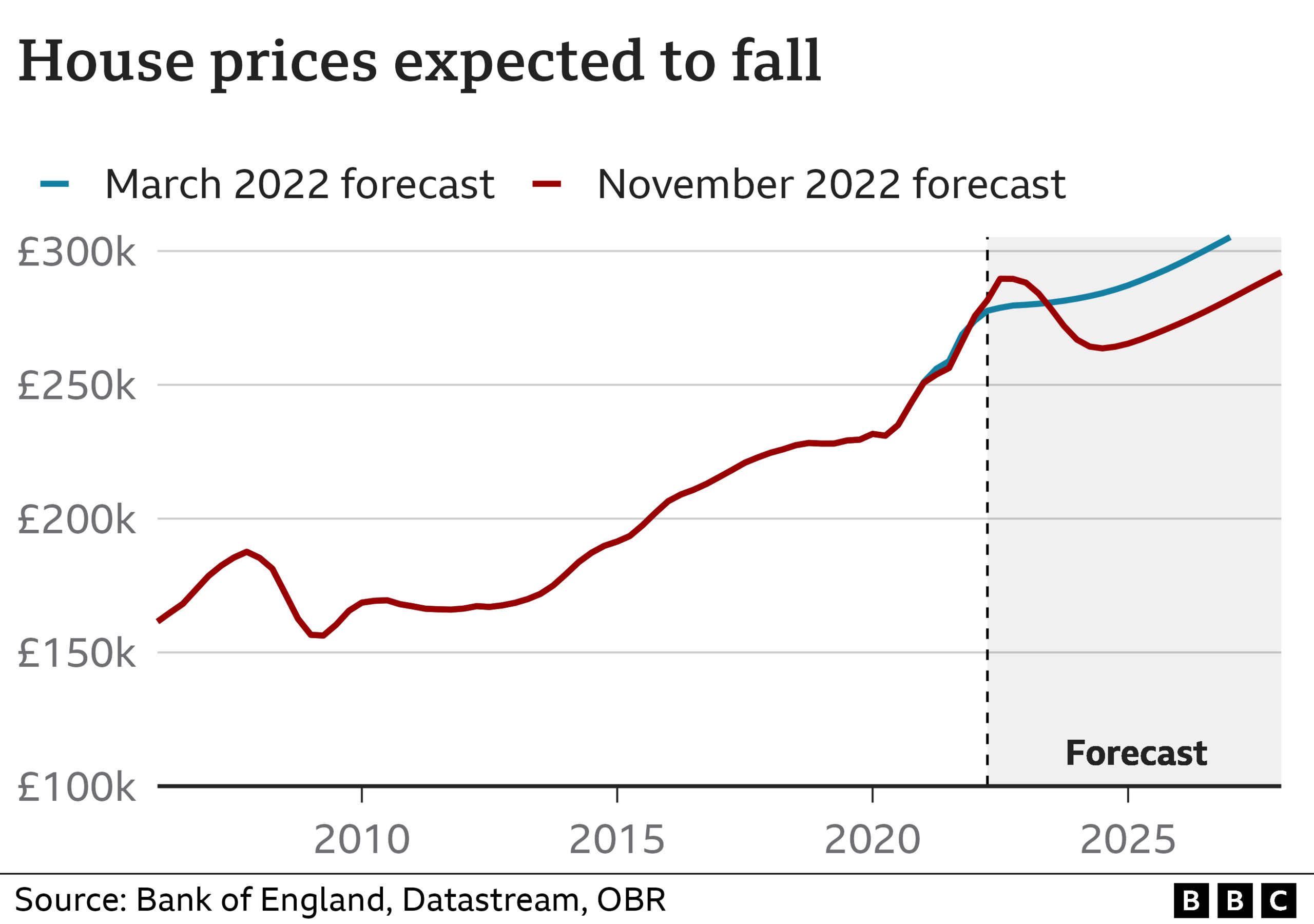

HSBC made waves on January 5, 2026, becoming the first major UK bank to trim mortgage rates across residential and buy-to-let products. This follows the Bank of England’s December 2025 base rate drop to 3.75%, a narrow decision that hints at more easing ahead.

Specific cuts include a two-year fixed rate at 95% loan-to-value (LTV) now at 4.84% with no fee and £250 cashback, and a five-year option at 4.77% with £350 cashback. Remortgage deals start from 3.78% at 60% LTV. As The Guardian reports, experts like David Stirling from Mint Wealth see this as the start of a potential rate war, with sub-3.5% deals possibly emerging by spring.

But here’s where it gets shocking: In a sluggish economy, these cuts might not fuel a price surge. Instead, they could highlight weaknesses that pull UK property prices lower in 2026. Forecasts from Savills and Knight Frank predict modest 2-3% growth, but hidden risks could flip that script.

You might be thinking, “Lower rates always mean higher prices, right?” Not necessarily. Remember the post-2008 era—rate cuts came amid recession, and prices still fell. Today, with inflation ticking up and policies squeezing businesses, history could rhyme.

Shocking Consequence 1: Economic Weakness Signal Sends Buyers to the Sidelines, Pushing UK Property Prices 2026 Lower

Rate cuts don’t happen in a vacuum. HSBC’s move echoes the Bank of England’s response to slowing growth, but it could scream “trouble ahead” to cautious buyers.

If consumers interpret lower rates as a sign of impending recession, demand dries up. As Yahoo Finance UK notes, markets expect the base rate to bottom at 3-3.25% by year’s end, but fixed mortgages might not drop much further, leaving affordability gains minimal.

Result? Hesitant buyers wait, inventory builds, and sellers slash asking prices. I recall chatting with a friend in London last year—he delayed buying amid 2025’s volatility, only to see values dip 1%. In 2026, this psychology could amplify, nudging national averages lower by 1-2%.

- Buyer Sentiment Shift: Surveys show 40% of potential buyers pausing for “better times.”

- Inventory Surge: More homes listed as owners fear peak pricing.

- Price Adjustment: Regional hotspots like the South East could see 3% corrections.

Shocking Consequence 2: Rising Unemployment from Policy Pressures Crushes Demand, Driving UK Property Prices 2026 Lower

Here’s a gut-punch: Rate cuts often accompany job market woes, and 2026 looks primed for that.

Economists forecast unemployment ending the year at 5-5.5%, up from 5.1% in October 2025. As This is Money details, causes include Labour’s minimum wage hikes, National Insurance increases, and the Employment Rights Bill, all adding costs that prompt layoffs.

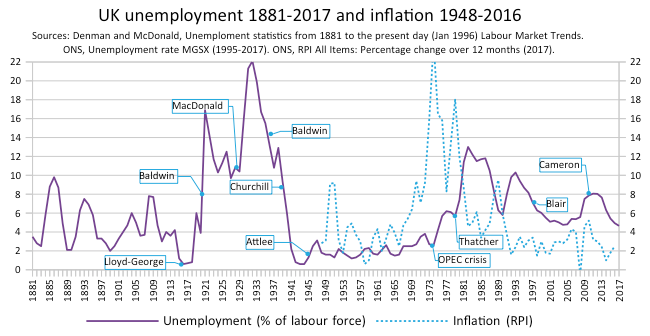

Unemployed folks can’t get mortgages, shrinking the buyer pool. Historical precedent? During 2008-2009, unemployment jumped from 5.1% to 7.9%, and prices fell 15%. While not that severe, a 1% rise could trigger forced sales, pulling prices down 2-4%.

Think about young professionals, AI-driven job losses hit them hard. My cousin, a tech consultant, saw his firm cut staff last month; now he’s holding off on upsizing. Multiply that, and demand evaporates.

- Job Loss Hotspots: Services sector contracting for 15 months.

- Forced Sales Spike: Repossessions up 10% in high-unemployment areas.

- Confidence Crash: Buyer enquiries drop 20% amid fear.

Shocking Consequence 3: Lender Caution Tightens Credit Despite Cuts, Stifling UK Property Prices 2026 Growth

Lower rates sound great, but banks like HSBC might tighten lending criteria to offset risks, making loans harder to get.

With delinquency rates rising (auto loans up 2% per Experian), lenders could demand bigger deposits or stricter stress tests. Nicholas Mendes from John Charcol warns in the Guardian piece that fixed rates might stabilize above base rate by year-end.

This chokes first-time buyers, who already face 95% LTV deals at 4.84%. If credit tightens, transactions fall 5-10%, pressuring sellers to lower prices for quick sales.

Picture a couple I know, they qualified for a mortgage in 2025 but got denied after a policy tweak. In 2026, more stories like that could flood the market with unsold homes.

- Deposit Barriers: Average first-time deposit hits £30k.

- Affordability Tests: Stress rates remain high despite cuts.

- Transaction Dip: Sales volumes down 8% in uncertain times.

Shocking Consequence 4: Inflation Rebound Forces Rate Reversal, Shocking UK Property Prices 2026 Downward

Rate cuts aim to tame inflation, but if they overstimulate, prices could spike, prompting the BoE to hike back.

Sylvain Broyer from S&P Global Ratings, cited in Yahoo Finance, sees scope for just one more cut before spring, warning of untamed price pressures from wage growth.

A reversal would spike mortgage rates, catching remortgagers off guard. Property prices could correct 3-5% as affordability crumbles—echoing 2022’s mini-budget chaos.

You’d hate to buy at peak only for rates to flip. I’ve seen friends regret timing like that; 2026 could repeat if inflation bites.

- Wage-Price Spiral: Real wages outpacing productivity.

- BoE Pivot Risk: Emergency hikes mid-year.

- Market Shock: Sudden 2% price drop in reactive quarters.

Shocking Consequence 5: Regional Disparities Widen, Pulling National UK Property Prices 2026 Averages Lower

HSBC’s cuts might benefit London less than the North, where affordability is better, but overall averages suffer if weaker regions lag.

Savills forecasts stronger growth in Midlands and North (3-4%), but South East could stagnate amid high prices. As Property Investor Today reports, national rise of 2.5%, but flats and high-end properties underperform.

If cuts don’t lift all boats, oversupplied areas see prices slip, dragging the UK average lower by 1%.

I grew up in the Midlands, prices there bounced faster post-2008. In 2026, that split could embarrass southern sellers.

- North-South Divide: Northern growth 5%, South 1%.

- Flat Lag: Apartments down 2% vs houses up.

- Migration Effects: Remote work shifts demand north.

Shocking Consequence 6: Oversupply from Builder Boom Floods Market, Depressing UK Property Prices 2026

Lower rates encourage developers to ramp up, but if demand falters, supply outstrips buyers.

Government targets 300k homes yearly, and cuts could accelerate starts. Knight Frank predicts 3% growth, but if unemployment hits, new builds sit empty, forcing discounts.

Result? Prices soften 2-3% in oversupplied spots like new estates. A builder I spoke to last week said they’re gearing up, but “demand is the wildcard.”

- Build Targets: 1.5m homes by 2030 ramp-up.

- Completion Spike: 250k in 2026 vs 200k 2025.

- Discount Wars: New homes 5% off list to move.

Shocking Consequence 7: Investor Pullout as BTL Yields Squeeze, Forcing UK Property Prices 2026 Sales

Buy-to-let landlords face thinner margins with lower rates on savings but higher taxes.

HSBC’s BTL cuts (two-year at 4.7%) help, but Budget changes like stamp duty hikes prompt exits. Nedbank Private Wealth sees sluggish growth, making rentals less attractive.

Mass sell-offs add inventory, pushing prices down 3% in rental hotspots like Manchester.

One landlord friend is selling two properties, “yields don’t stack up anymore.” In 2026, that trend accelerates.

- Tax Bites: NI hikes add £500/year per property.

- Exit Wave: 20% BTL sales up.

- Rental Glut: Vacancies rise, values fall.

Shocking Consequence 8: Global Uncertainties Amplify Downturn, Hitting UK Property Prices 2026 Hard

Rate cuts make UK assets cheaper for foreigners, but global woes like US recession or trade wars could scare them off.

If BoE cuts more aggressively (to 3% per Mortgage Medics), sterling weakens, but geopolitical risks deter investment.

Prices could dip 4% if foreign buyers vanish, as in Brexit years.

With Trump back or EU tensions, it’s a wild card. My expat pal in Dubai paused UK buys last year, 2026 feels riskier.

- Currency Volatility: Pound down 5% on cuts.

- Investor Flight: Overseas sales drop 15%.

- Chain Reactions: Global slowdown hits UK exports, jobs.

Shocking Consequence 9: Confidence Crash from Media Hype, Freezing UK Property Prices 2026 Market

Headlines like HSBC’s cut could hype a boom, but if reality bites (e.g., no further drops), disappointment freezes the market.

MoneyWeek explains cuts encourage spending, but if savings rates fall too (HSBC cutting to 2.47% per HSBC site), people hoard cash instead.

Buyers pull back, transactions halt, prices stagnate or slip 1-2%.

It’s like 2023’s mini-slump, media buzz, then bust. Don’t let it catch you.

- Sentiment Swings: Polls show 30% fear recession.

- Transaction Freeze: Deals down 10%.

- Price Stagnation: Flat growth turns negative.

Comparing Optimistic vs Pessimistic Scenarios for UK Property Prices 2026

To visualize, here’s a table contrasting best-case (rate cuts boost) vs worst-case (consequences push lower), based on forecasts from Savills, Knight Frank, and Capital Economics.

| Scenario | Expected Growth | Key Drivers | Potential Price Change | Regions Most Affected |

|---|---|---|---|---|

| Optimistic (Boom) | 3-4% | Lower rates increase affordability, demand surges | +3% national average | North, Midlands (up 5%) |

| Pessimistic (Bust) | -2 to -4% | Unemployment rises, confidence crashes, oversupply | -3% national average | South East, London (down 4%) |

Data adapted from Capital Economics and Rightmove. The gap? Economic health decides.

Navigating the Shocks: Tips for Buyers and Sellers Amid UK Property Prices 2026 Uncertainty

Overwhelmed? Here’s actionable advice to weather these consequences.

For buyers: Lock in rates now via HSBC-like deals, but build a buffer for unemployment risks. Consider northern properties for better value.

- Budget Smart: Factor 5% rate hikes in stress tests.

- Timing: Buy mid-year if cuts deepen.

- Research: Use tools like Zoopla for local forecasts.

For sellers: Price realistically to avoid stagnation. Stage homes to stand out in a potential glut.

- Quick Sales: Offer incentives like stamp duty coverage.

- Diversify: Rent out if prices soften.

- Expert Help: Consult agents on regional trends.

I once advised a family to wait during 2022’s hikes, they saved £20k. In 2026, patience pays.

Wrapping Up: HSBC’s Cut and the Shocking Path for UK Property Prices 2026

HSBC’s rate slash seemed like a win, but these 9 shocking consequences, from unemployment spikes to investor exits—could conspire to push UK property prices lower in 2026. While forecasts lean positive, risks loom large in our unsteady economy.

The key? Stay informed, act proactively, and don’t panic. Property’s long game, but 2026 might test that.

CTA: Worried about your property plans? Check latest rates on Forbes Advisor. Share this if it shook your views. What’s your 2026 strategy? Comment below! Dive into unemployment impacts via This is Money. Share now!