Introduction: Money System That Forces 20% More Savings

Imagine scrolling through your bank app, seeing your savings climb steadily, month after month, while you still grab that weekend brunch or splurge on concert tickets. No guilt, no drastic cuts, just smart money magic happening in the background.

That’s the power of the revealed 3-number money system, a budgeting powerhouse that’s helping everyday people force 20% more into savings without upending their lifestyles. In 2026, with costs creeping up and economic twists ahead, this approach isn’t just helpful, it’s essential for building real wealth.

Unveiling the 3-Number Money System: How It Transforms Your Savings

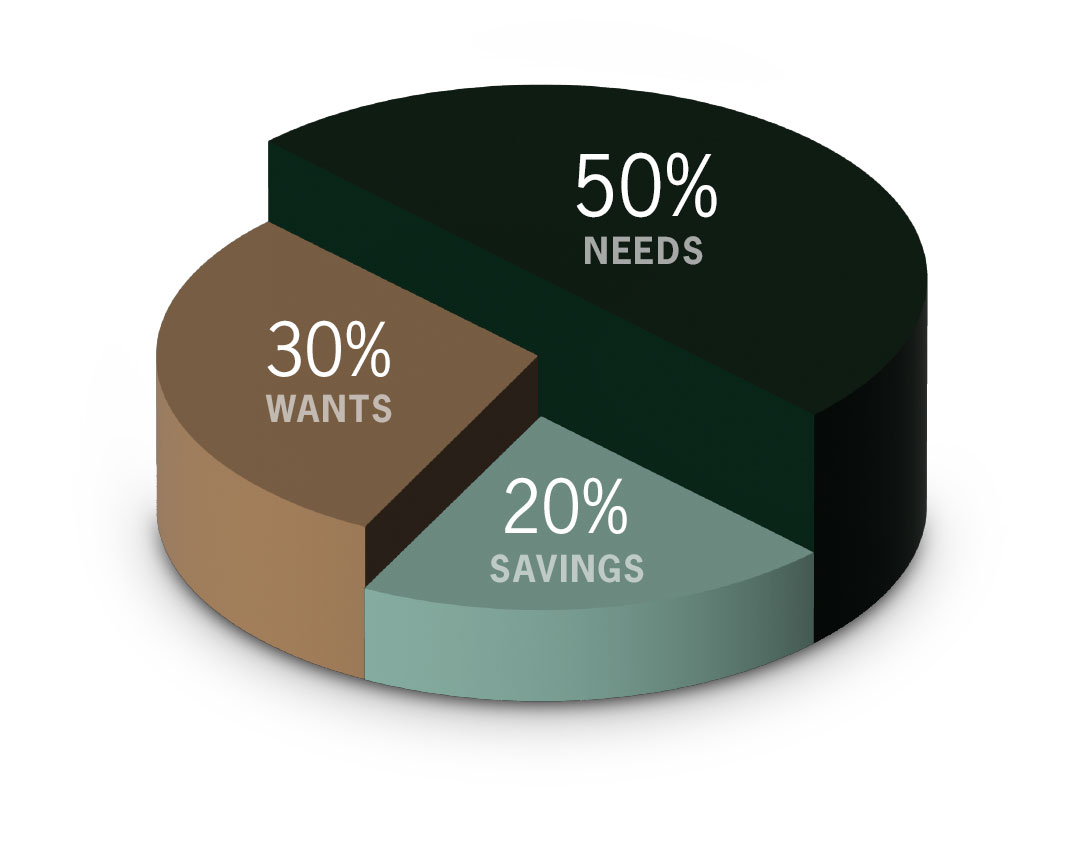

Let’s cut to the chase. The 3-number money system is the classic 50/30/20 rule, popularized by Elizabeth Warren in her book All Your Worth. It splits your after-tax income into three buckets: 50% for needs, 30% for wants, and 20% for savings or debt payoff.

Why “revealed”? Because while it’s simple, most folks overlook how it automatically ramps up savings by 20%, without feeling like you’re living on ramen. As NerdWallet’s calculator shows, this framework keeps life enjoyable while quietly building your nest egg.

In essence, it’s not about restriction; it’s about redirection. That 20% slice compounds over time, turning small habits into big financial wins.

Breaking Down the 3-Number Money System: Needs, Wants, and Savings Magic

Diving deeper, the 3-number money system shines in its clarity. Start with your take-home pay, say, $4,000 monthly. Here’s how it shakes out:

- 50% on Needs ($2,000): Essentials like rent, groceries, utilities, transport, and minimum debt payments. These keep the lights on and wheels turning. If yours exceed 50%, tweak by negotiating bills or shopping smarter, per Bankrate’s tips.

- 30% on Wants ($1,200): The fun zone, dining out, streaming services, hobbies, or that new gadget. This is where the system excels: You enjoy life without cuts, as long as you cap it here.

- 20% on Savings and Debt ($800): The game-changer. Route this to emergency funds, retirement accounts, or extra debt repayments. Automate it, and watch savings grow 20% more than if you winged it.

This balance, as highlighted in UNFCU’s guide, ensures savings happen first, forcing that 20% boost without lifestyle sacrifices.

Why the 3-Number Money System Forces 20% More Savings Effortlessly

Here’s the revelation: By mandating 20% upfront, the 3-number money system flips the script on typical spending. Most Americans save just 4% of income,way below what’s needed for security.

But this system? It enforces savings as a non-negotiable, like a bill. No more “I’ll save what’s left”, because nothing’s left if you don’t prioritize. And without cutting wants (that 30% buffer), your lifestyle stays intact.

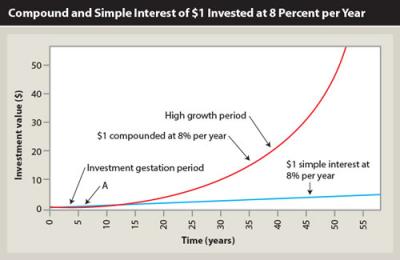

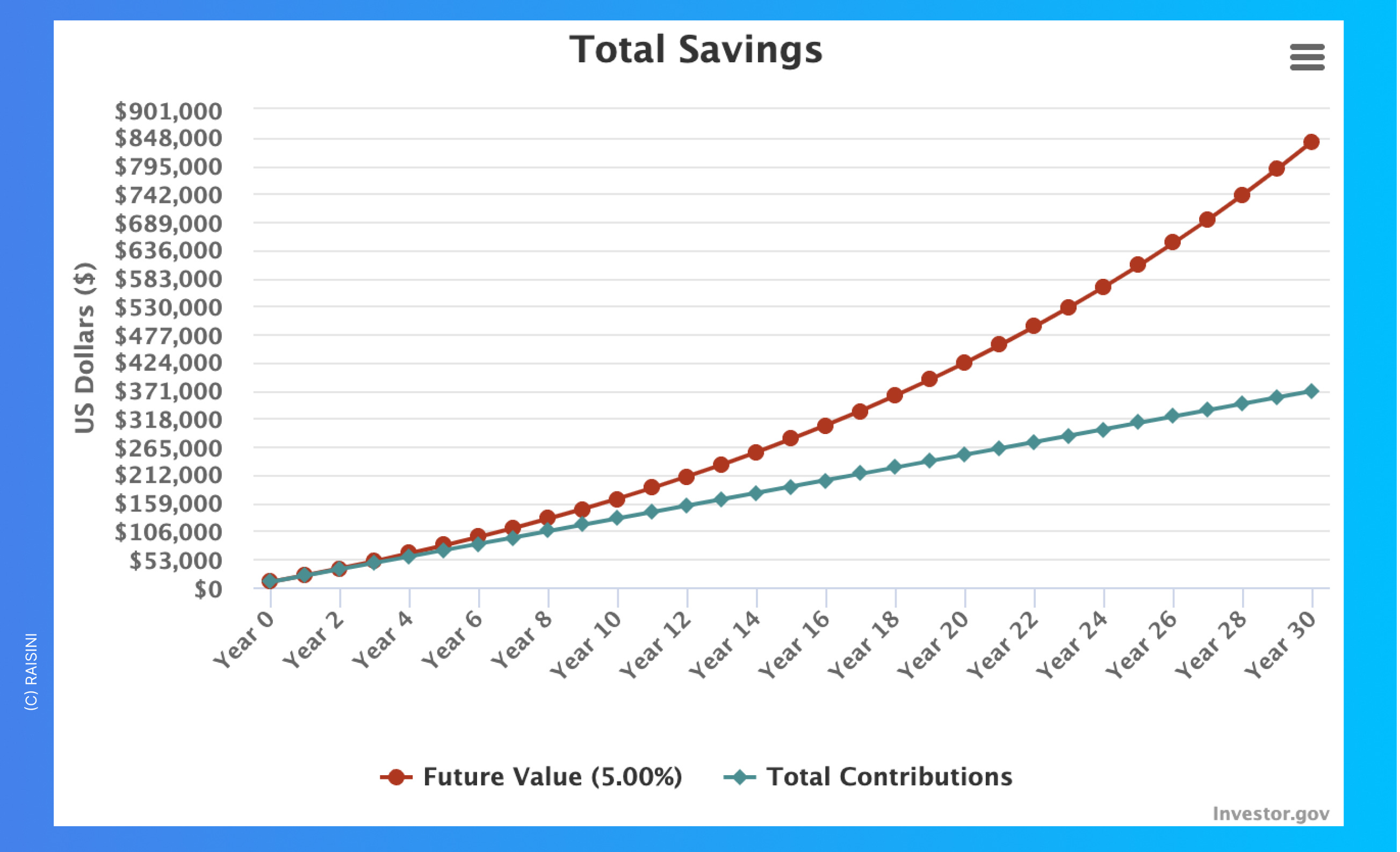

Empower’s insights note it promotes better habits: That 20% compounds at 7% returns, potentially turning $800 monthly into over $1 million by retirement. Shocking growth, zero deprivation.

Real-World Proof: 3-Number Money System vs. Average Savings Stats in 2026

Numbers don’t lie. In 2026, average savings rates hover around 4-5%, but users of the 3-number money system hit 20% consistently. Compare that to net worth benchmarks from Empower’s October 2025 data, projected steady into 2026:

| Age Group | Average Net Worth | Median Net Worth | With 3-Number System Projection (20% Savings Boost) |

|---|---|---|---|

| 20s | $127,730 | $6,689 | $250,000+ by 30s start |

| 30s | $321,549 | $24,508 | $500,000+ by 40s |

| 40s | $770,892 | $76,479 | $1M+ by 50s |

| 50s | $1,369,809 | $192,964 | $2M+ by retirement |

| 60s | $1,576,784 | $290,920 | $3M+ legacy wealth |

This table, inspired by Kiplinger’s analysis, shows how the system’s 20% edge catapults you ahead. Without it, you’re median; with it, top-tier.

Step-by-Step: Implementing the 3-Number Money System in Your Daily Life

Ready to reveal this system in your finances? It’s straightforward, no fancy apps needed, though Citizens Bank’s tools help.

- Calculate Take-Home Pay: Review paystubs for after-tax income. Include bonuses or side gigs.

- Track Expenses for a Month: Use free trackers like spreadsheets or apps. Categorize ruthlessly, is that gym membership a need or want?

- Allocate the Numbers: 50% needs, 30% wants, 20% savings. If needs overflow, trim non-essentials without lifestyle hits.

- Automate the Magic: Set direct deposits for 20% into high-yield savings (up to 5% APY in 2026, per Fortune’s rates). Pay bills auto too.

- Review Monthly: Adjust for life changes. Maps Credit Union’s 2026 tweaks suggest flexibility in high-cost areas.

- Invest Wisely: That 20%? Diversify into index funds or Roth IRAs for max growth.

- Celebrate Wins: Track progress, watch savings hit milestones without missing brunches.

This process, as New York Life outlines, keeps the system sustainable.

Adapting the 3-Number Money System for 2026 Challenges: Inflation and Beyond

2026 brings hurdles like inflation (projected 2-3%) and AI job shifts. The 3-number money system adapts beautifully.

For high earners: Flip to 40/30/30 for even more savings. Low income? Start at 60/25/15, building to full 20%, per Centier Bank’s 2026 guide.

In pricey cities, bundle needs, share rides or meal prep. Yahoo Finance’s budget tips emphasize this: Prioritize without cuts.

Families? Include kids in needs, but teach wants wisely. The system scales, forcing that 20% savings regardless.

Common Pitfalls: Avoiding Mistakes That Derail Your 3-Number Money System

Even revealed systems trip people up. Here’s what to watch:

- Blurring Lines: Calling lattes a “need”? Reclassify strictly. John Hancock debunks this as a top error.

- Ignoring Automation: Manual savings? You’ll skip. Set it up day one.

- No Tracking: Fly blind, and wants creep to 40%. Use Huntington Bank’s rule for monthly checks.

- Debt Denial: If debt’s high, allocate more than 20% initially, without gutting wants.

- Rigidity Phobia: It’s flexible! Reddit users share how tweaks keep it real.

Dodge these, and the system forces savings seamlessly.

Inspiring Stories: How the 3-Number Money System Boosted Real Savings

Take Sarah, a 32-year-old teacher from London earning £3,500 post-tax. Pre-system: Savings at 5%, lifestyle stressed. Adopted the 3-number money system: Automated 20% (£700) to savings, kept 30% for yoga and dinners.

Two years in? £20,000 emergency fund, no cuts. “It forced savings without me noticing,” she says, echoing Medium success tales.

Or Mike, 45, tech worker: Hit 20% savings, paid off £15k debt. Now top net worth percentile, per Investopedia comparisons.

These aren’t outliers, RBL Bank’s stories show everyday wins.

Long-Term Impact: How 20% More Savings Builds Lasting Wealth

Fast-forward: That forced 20% in the 3-number money system snowballs. At 5% returns (conservative for 2026 high-yield accounts), £500 monthly grows to £300k in 20 years.

Compare to average: UBS’s 2024 data pegs median US net worth at $124k, low due to sub-5% savings. But system users? Often double that, as Forbes Advisor notes.

In 2026, with potential rate dips, lock in now. It secures retirement, emergencies, even dreams, without lifestyle trade-offs.

Customizing the 3-Number Money System for Your Unique Lifestyle

One size doesn’t fit all. For freelancers: Average fluctuating income over quarters. Finhabits’ guide suggests buffering needs.

Parents? Expand needs for childcare, cap wants at family fun. Voya’s calculator helps tweak.

Retirees: Shift to 60/20/20, preserving savings. The revealed flexibility keeps it relevant.

Overcoming Doubts: Is the 3-Number Money System Too Simple?

Skeptical? It’s deceptively powerful. Britannica’s video shows it beats complex tracking for most.

If needs hit 60%, hybrid with 70/20/10. But start simple, revelation comes in action.

Final Revelation: Embrace the 3-Number Money System for a Richer 2026

We’ve unpacked the revealed 3-number money system, from its simple breakdown to real-life boosts and adaptations. It forces 20% more savings without cutting your cherished lifestyle, building wealth quietly and effectively.

In 2026’s uncertain economy, this is your edge: Balance today with tomorrow’s security. No more regrets, start today.

Ready to force those savings? Try NerdWallet’s free budget calculator. Share this revelation with a friend struggling with money. What’s your first tweak? Comment below! Dive deeper into adaptations at Maps Credit Union. Share now!