Introduction: The shocking inflation math which shows you’re losing money everyday.

You log into your banking app, see that steady balance in your checking account, and breathe a sigh of relief, it’s safe, right? But here’s the gut punch: While you’re feeling secure, inflation is silently chipping away at your money’s value every single day, especially with that 0% APY doing nothing to fight back.

In January 2026, with inflation hovering around 2.7% based on the latest US Inflation Calculator data, your “safe” checking account isn’t protecting you, it’s costing you. Let’s unpack this shocking reality and show you how to turn it around before more purchasing power slips away.

The Shocking Inflation Math: How 0% APY in Your Checking Account Erodes Wealth

Think about it, your checking account feels like a fortress, always there for bills and emergencies. But without interest, it’s more like a leaky bucket. Inflation, the rise in prices over time, means $100 today buys less tomorrow. At 2.7%, as reported in November 2025 by the Bureau of Labor Statistics, your money loses about 2.7% of its buying power annually.

No APY? You’re down that full amount. Have $10,000 sitting idle? That’s roughly $270 gone in a year, just vanished into higher grocery bills or rent hikes. Shocking, isn’t it? As Investopedia explains, this erosion happens quietly, but over years, it adds up to thousands in lost value.

And it’s not just theory. With the average traditional checking account yielding a measly 0.07% APY according to Forbes Advisor, most Americans are in this boat, watching their hard-earned cash diminish without a fight.

Why Traditional 0% APY Checking Accounts Are a Silent Wealth Killer in 2026

We’ve all been there, stashing extra cash in checking because it’s convenient. No withdrawal limits, easy access, FDIC-insured up to $250,000. Feels safe, right? But in 2026’s economy, where AI-driven jobs and rising costs dominate, that safety is an illusion.

The shocking inflation math reveals the truth: Low or zero interest means your money isn’t growing, while everything else is getting pricier. A PNC Insights article highlights how even a 1% APY account loses 2% real value at 3% inflation. At 0%, it’s worse, pure loss.

Billions are parked in these accounts. Recent stats from the Federal Reserve show households hold massive sums in low-yield spots, transferring wealth to banks via fees and loans. You’re essentially lending your money for free while inflation nibbles away.

Breaking Down the Shocking Inflation Math: Real Numbers on Your 0% APY Losses

Let’s crunch the shocking inflation math with real examples. Suppose you have $20,000 in a 0% APY checking account. At 2.7% inflation, after one year, its real value drops to about $19,460—$540 lost to eroded purchasing power.

Over five years? Assuming steady 2.6% inflation (projected for 2026 by Trading Economics), that $20,000 shrinks to around $17,500 in today’s dollars. Shocking, right? You’re losing over $2,500 without touching a dime.

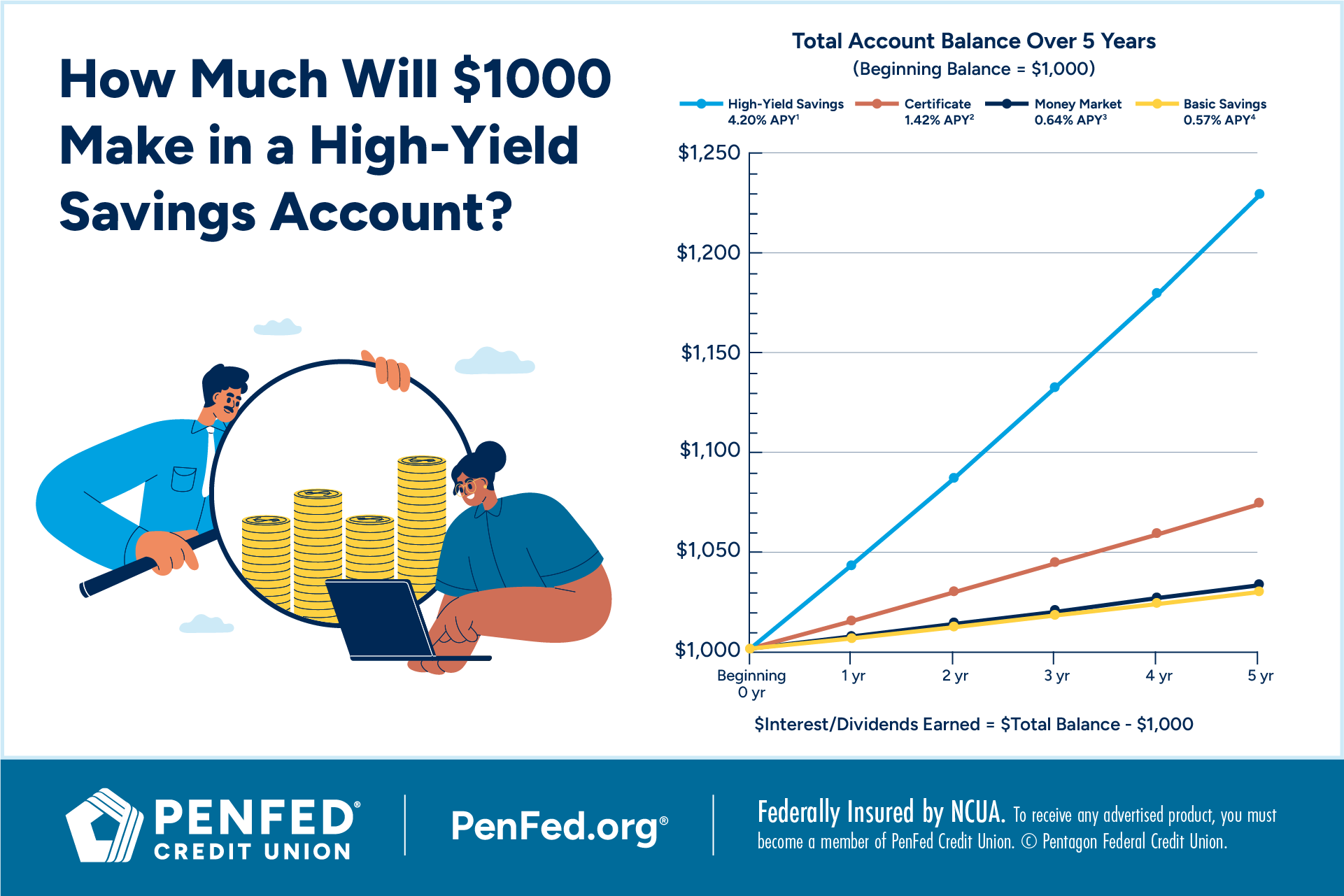

Compare that to a high-yield savings account at 4.20% APY, like those from Peak Bank. Not only do you beat inflation, but you gain. The same $20,000 could grow to $22,300 nominally, preserving and boosting real value.

To visualize, here’s a simple table comparing $10,000 in a 0% APY checking account vs. a 4.00% HYSA over five years at 2.7% average inflation:

| Year | 0% APY Checking (Nominal) | 0% APY Checking (Real Value) | 4.00% HYSA (Nominal) | 4.00% HYSA (Real Value) |

|---|---|---|---|---|

| 0 | $10,000 | $10,000 | $10,000 | $10,000 |

| 1 | $10,000 | $9,730 | $10,400 | $10,119 |

| 2 | $10,000 | $9,467 | $10,816 | $10,240 |

| 3 | $10,000 | $9,212 | $11,249 | $10,365 |

| 4 | $10,000 | $8,964 | $11,699 | $10,494 |

| 5 | $10,000 | $8,723 | $12,167 | $10,626 |

Calculations assume compound interest for HYSA and steady inflation adjustment. See how the checking account hemorrhages value? The HYSA? It fights back, per tools like Bankrate’s calculator.

Common Myths About 0% APY Checking Accounts and Shocking Inflation Realities

Myth one: “My money is safe from market risks.” True, but inflation is a risk too. As Forbes Advisor notes, even moderate inflation erodes cash faster than many realize.

Myth two: “I need liquidity, so checking is best.” Sure, but you can have both. Many high-yield options offer easy transfers. Don’t let convenience cost you.

Myth three: “Inflation isn’t that bad now.” With rates at 2.7% in late 2025 per YCharts, it’s steady erosion. Projections for 2026 from J.P. Morgan suggest it could tick up to 3.3% before settling, amplifying losses.

- Daily Impact: At 2.7%, $50,000 loses about $3.70 daily. Shocking when compounded.

- Long-Term Hit: Over 10 years, that’s $13,500 vanished from purchasing power.

- Who Suffers Most: Everyday folks with emergency funds idle, as Transcend Credit Union warns.

Shocking Statistics: Billions Lost in 0% APY Checking Accounts Amid Inflation

Here’s where it gets eye-opening. Americans hold trillions in low-interest accounts. A 2025 FDIC report estimates average savings rates at 0.39%, but checking often at 0.01%. With inflation at 2.7%, that’s a net loss for millions.

One study from Wealth and Finance pegs billions in annual erosion. High-net-worth folks? They avoid this, parking cash in 4%+ yields.

In 2026, as rates may dip per Investopedia’s outlook, low-APY traps worsen. Yet, only 20% use high-yield options, per surveys, leaving most vulnerable.

Alternatives to 0% APY Checking Accounts: Beat the Shocking Inflation Math

Enough doom, let’s flip the script. High-yield savings accounts (HYSAs) offer 4-5% APY, outpacing inflation. Top picks in January 2026:

- Varo Bank: 5.00% APY on up to $5,000, as listed by Investopedia.

- AdelFi: 5.00% APY, great for faith-based banking.

- Fitness Bank: 4.75% APY, rewarding active lifestyles.

These are FDIC-insured, liquid, and beat shocking inflation math handily. Money market accounts? Similar yields with check-writing. CDs lock in rates but limit access.

Why switch? A NerdWallet guide shows HYSAs multiply savings growth. For $10,000 at 4.35%, earn $435 yearly vs. $0 in checking, plus inflation protection.

Step-by-Step Guide: Moving from 0% APY Checking to Inflation-Beating Options

Ready to stop losing money? Here’s how:

- Assess Your Needs: Keep 1-2 months’ expenses in checking for bills. Move the rest.

- Research HYSAs: Use sites like Bankrate for current rates—aim for 4%+.

- Open an Account: Online banks like Ally or Capital One take minutes, no fees.

- Transfer Funds: Link accounts, automate deposits. Watch for bonuses—some offer $200+.

- Monitor Inflation: Track via Cleveland Fed’s nowcast—adjust as needed.

- Diversify: Mix HYSAs with investments for higher returns, but start safe.

- Review Annually: Rates change; shop around per WSJ Buy Side.

This beats the shocking inflation math, turning losses into gains. As I Will Teach You To Be Rich advises, automation is key, no effort, big rewards.

Real-Life Examples: Escaping the 0% APY Trap and Defeating Shocking Inflation

Take Sarah, a 35-year-old teacher with $15,000 in checking. Shocked by inflation math, she switched to a 4.5% HYSA. One year later? $675 earned, beating 2.7% inflation by $270 net gain.

Or Mike, retiree with $50,000 idle. Post-switch to American Express HYSA, he’s up $2,000 annually, funding trips without dipping principal.

These stories echo blogs like Due’s inflation impact piece, where folks regret waiting. Don’t be them, act in 2026.

Advanced Strategies: Beyond Basics to Maximize Against Shocking Inflation Math

For pros: Ladder CDs for locked rates, as CBS News forecasts flat 2026 yields. Or I-bonds tied to inflation.

Invest in stocks or ETFs for 7-10% historical returns, outrunning 2.7% erosion. But risk-averse? Stick to HYSAs.

Tax perks: Roth IRAs with high-yield options amplify. As Fidelity’s trends note, 2026’s side-hustle boom pairs well—funnel earnings to high-APY spots.

Potential Drawbacks: Is Ditching 0% APY Checking Always Right?

Fair question. HYSAs may have transfer delays (1-3 days), vs. instant checking. Some require minimums, like Openbank’s $500.

But pros outweigh: Beat inflation, earn passively. In low-rate 2026 per Forbes Advisor forecast, even 4% is a win over 0%.

If you’re high-risk tolerant, explore more, but for most, this curbs shocking losses.

The Bigger Picture: Shocking Inflation Math in a 2026 Economy

2026 brings uncertainties, potential rate drops to 2.9% per Wealthtender, AI job shifts. Your 0% APY checking? A liability.

By understanding this math, you’re empowered. As Al Jazeera reports, steady inflation means proactive saving is key.

Don’t let complacency cost you, rethink that “safe” account today.

Wrapping Up: Stop Losing Money to Shocking Inflation Math in Your 0% APY Checking Account

We’ve dissected the shocking inflation math, exposed 0% APY pitfalls, crunched numbers, and charted escapes. Your checking account feels safe, but it’s a slow leak in 2026’s economy.

The fix? Shift to high-yield alternatives, preserve, grow, thrive. Inflation won’t wait; neither should you.

CTA: Ready to beat inflation? Check top HYSAs at NerdWallet and open one today. Share this if it shocked you. What’s your plan? Comment below! Read more on rate forecasts? Visit Kiplinger. Share now!