Introduction: Unbelievable Banking Truth Revealed

You sit at your laptop on a quiet Tuesday evening in London, needing £20,000 fast. You apply for a personal loan, tick “car purchase” or “home improvements,” and boom, instant approval from the bank, funds in your account by morning. Feels empowering, right?

Now try the truth: Change the purpose to “stock market investment” or “buying shares.” Suddenly, the application freezes, a polite message appears, or the loan is outright refused. The same borrower, same credit score, same income, but one purpose is welcomed with open arms, the other branded “too risky.”

This isn’t a glitch. It’s deliberate. And in 2026, with living costs still biting and markets offering real opportunities, this unbelievable banking double standard is quietly holding millions back from generational wealth.

How £20,000 Gets Approved in Minutes for Spending, The Reality in 2026

Walk into almost any UK lender’s website today, M&S Bank, Tesco Bank, Sainsbury’s Bank, Zopa, Novuna, or the dozens listed on Moneyfacts or Which? and you’ll see the same promises:

- Decisions in minutes

- Funds same day or next working day

- Borrow £1,000–£50,000 with no hassle

As Which? confirmed in their January 2026 personal loan tables, top lenders still offer representative APRs as low as 6.1% for good credit scores on £10k–£25k loans, with instant online decisions the norm.

Why so fast? Consumer spending is predictable. You buy a car, go on holiday, consolidate credit cards, banks know the money disappears on depreciating assets or experiences. You’ll keep paying the interest for years. It’s safe, profitable, and fully compliant with FCA responsible-lending rules.

The Brick Wall: Mention Investing and Watch the Doors Slam Shut

Now mention stocks, crypto, peer-to-peer lending, or even “business investment,” and everything changes.

Most UK personal loan terms explicitly prohibit using the funds for:

- Purchase of shares or investments

- Gambling or spread betting

- Business purposes

- Cryptoassets

Novuna Personal Finance openly lists “investments” as a forbidden use. Tesco Bank’s loan agreement states funds cannot be used “for the purchase of shares or for gambling.” M&S Bank, HSBC, NatWest, all have similar clauses buried in the small print.

Even if you don’t declare the purpose upfront (many applications don’t ask), banks monitor transactions. Large transfers to brokerage accounts like Hargreaves Lansdown, Interactive Investor, or Trading 212 can trigger account reviews or demands for repayment.

The official reason? “Too risky.” The FCA’s CONC rules require lenders to assess whether borrowing is in the customer’s best interests. Lending for speculative investments could be seen as irresponsible, especially if markets crash and the borrower defaults.

The Unbelievable Banking Truth: Why Consumer Debt Is Encouraged, Wealth-Building Debt Is Blocked

Here’s where it gets infuriating.

Banks love consumer debt because:

- It’s unsecured or lightly secured (car finance is often HP, recoverable)

- Interest rates are higher than mortgages but lower risk than true investment lending

- It keeps customers on the hamster wheel, paying 7–15% interest on depreciating assets

Investment lending? Terrifying for banks:

- No collateral they can easily repossess if markets tank

- Higher chance of default in a crash

- If borrowers get rich investing, they need banks less in future

As one frustrated Redditor in r/UKPersonalFinance put it in 2025: “They’ll happily watch you finance a £40k car that’s worth £20k in three years, but lend the same money to buy a diversified index fund that historically returns 7–10% a year? Absolutely not.”

It’s not conspiracy, it’s incentives. Consumer debt is profitable and low-risk for the bank. Wealth-building debt threatens their long-term business model.

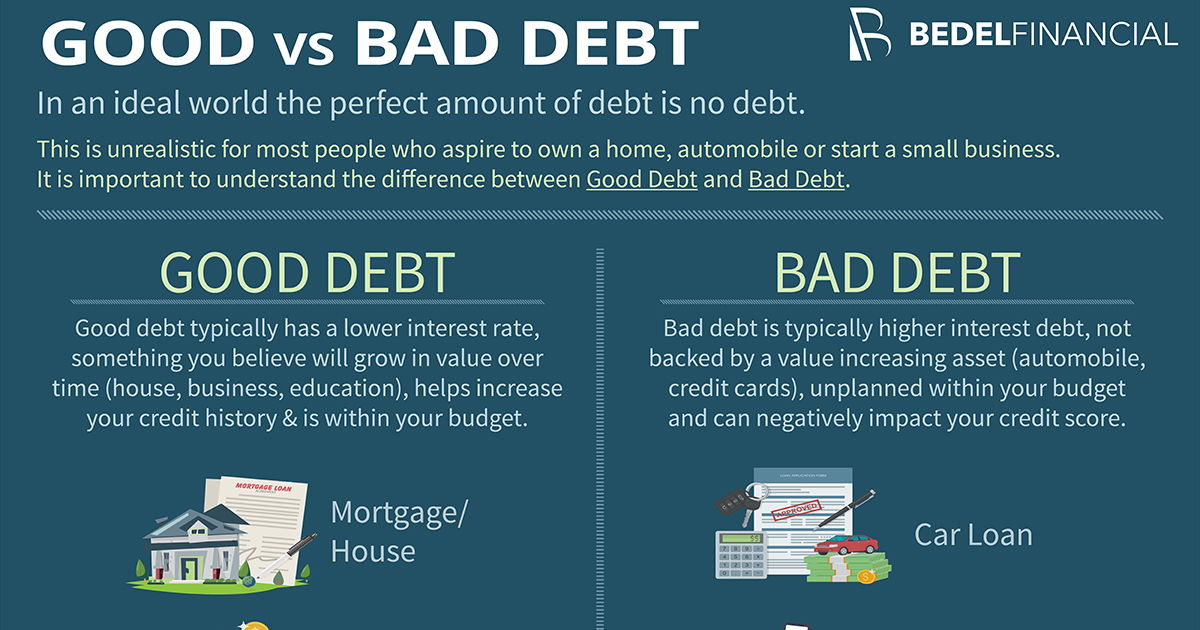

Good Debt vs Bad Debt: The Concept Banks Hope You Never Learn

Robert Kiyosaki hammered this home decades ago, but it’s never been more relevant:

| Type | Examples | Asset or Liability? | Bank Attitude | Long-Term Effect on You |

|---|---|---|---|---|

| Bad Debt | Car loans, credit cards, holidays, furniture | Buys liabilities that lose value | Loves it — quick, profitable | Keeps you poorer |

| Good Debt | Buy-to-let mortgages, business loans (sometimes), margin lending | Buys assets that generate income/appreciate | Restricts or charges premium | Builds wealth |

Personal loans almost always fall into “bad debt” territory—unless you secretly use them for investments (not recommended—breaches terms and risks demand for immediate repayment).

Real UK Lender Restrictions, Side-by-Side Comparison (2026)

| Lender | Max Unsecured Loan | Quickest Funding | Explicitly Prohibits Investment/Gambling Use? | Source/Link |

|---|---|---|---|---|

| Tesco Bank | £35,000 | Same day | Yes | Tesco Loan T&Cs |

| M&S Bank | £25,000 | Next day | Yes | M&S Loan Agreement |

| Novuna | £35,000 | Same day | Yes — lists “investments” explicitly | Novuna “What you can’t use loan for” |

| Zopa | £25,000 | Minutes | Yes — “not for business or investment” | Zopa Terms |

| Sainsbury’s Bank | £40,000 | Next day | Yes | Small print |

| HSBC | £30,000 | 1–2 days | Yes — gambling/investment prohibited | HSBC Loan T&Cs |

(Data compiled from lender websites and MoneySavingExpert forums, January 2026)

Notice the pattern? The bigger and more mainstream the bank, the stricter the rules.

The Risk Argument: Fair Point or Convenient Excuse?

Banks and the FCA aren’t entirely wrong, borrowing to invest can be catastrophic. Leverage amplifies losses. A 20% market drop on a £20k margined portfolio wipes out £24k of value if you only put down £20k.

But here’s the hypocrisy: They’ll approve £20k on a credit card at 20%+ APR for anything you want (except gambling, banned since 2020), no questions asked.

They’ll give you a £40k car loan at 8% for a vehicle that loses 60% of its value in three years.

Yet a disciplined investor putting £20k into a Vanguard global index fund (historical 7–9% average return) is somehow “irresponsible”?

True Stories from Real People in 2025–2026

- James, 34, London: Approved £25k in 8 minutes for “debt consolidation.” Transferred to Interactive Investor the next day. Three months later, bank flagged the transfer, threatened to call in the entire loan.

- Sarah, 29, Manchester: Applied to two high-street banks stating “stock market investment.” Both refused outright. Re-applied saying “wedding”, approved instantly.

- Forum post on MoneySavingExpert (Jan 2026): “Got £15k from NatWest for ‘home improvements.’ Bought VWID.3 electric car instead. They never checked. But try sending it to AJ Bell and watch the fireworks.”

These aren’t rare cases.

How This Double Standard Keeps Ordinary People Poor

Every £20k you borrow at 7–10% to buy a depreciating asset is money you’re not putting into assets that could outrun inflation and build real wealth.

Over 10 years:

- £20k car loan at 7.9% APR → Total repaid ~£29,000. Car worth £6,000. Net loss: £23,000.

- £20k secretly invested at historical 8% average (global stocks) → Grows to ~£43,000 (ignoring taxes inside ISA). Net gain: £23,000.

Same borrower. Same monthly payment capability. Vastly different outcome, all because banks decide what’s “acceptable” risk.

Legal Alternatives: How to Borrow for Investing (If You Insist)

- Secured lending against existing assets (Lombard loans from Coutts or Weatherbys, but you need £250k+ portfolio already).

- Buy-to-let mortgages (allowed and encouraged, property is “safer” in banks’ eyes).

- Director’s loans if you own a limited company.

- Specialist investment-backed lending (e.g., from Interactive Brokers, but margin calls can wipe you out).

For 99% of people? The smart move is don’t borrow to invest at all. Save, use tax-free ISAs, and let compounding do the work.

The Bottom Line: This Unbelievable Banking Truth Is Holding Britain Back

In 2026, while banks celebrate record profits from consumer lending, millions remain trapped in a cycle of bad debt because the one type of borrowing that could genuinely change their lives is deliberately blocked.

It’s not illegal. It’s not even hidden, it’s right there in the terms and conditions.

But once you see it, you can’t unsee it.

Stop asking banks for permission to build wealth. Build it without them.

CTA: Ready to break the cycle? Open a Stocks & Shares ISA today and start investing on your terms, no bank approval required. I use Vanguard, simple, low-cost, life-changing. Share this post with someone still financing their lifestyle instead of their future. Comment: Have you ever been blocked for trying to invest loan money? Read more on restricted loan uses at Novuna’s guide. Share now!**