Introduction: 10-Year Delay That Can Destroy 52% of Your Retirement

Imagine turning 65, ready to kick back on that dream beach, only to realize your nest egg is half what it could have been, all because you hit “snooze” on saving for a decade back in your 30s. Sounds like a nightmare, right? But this isn’t fiction; it’s the harsh reality of compound interest’s unforgiving math that most young adults brush off until it’s too late.

In 2026, with economic uncertainties like AI job shifts and lingering inflation, understanding this 10-year retirement delay isn’t just smart—it’s essential. Stick with me as we unpack the shocking numbers, real stories, and actionable steps to safeguard your future.

What Is the 10-Year Retirement Delay and Why It Matters in 2026

Let’s break it down simply. The 10-year retirement delay refers to postponing serious savings from, say, age 30 to 40. It might feel harmless, life’s busy with careers, kids, or loans, but the math shows it can slash your retirement fund by over half.

Why? Compound interest. Your money earns returns, and those returns earn more returns, snowballing over time. A decade less means missing prime growth years. As Vanguard’s retirement guide explains, early starters leverage time as their biggest ally.

In today’s world, with longer lifespans pushing retirement past 65, ignoring this delay risks working forever or scaling back dreams. But knowledge is power, let’s dive into the numbers.

The Unbelievable Math Behind the 10-Year Retirement Delay

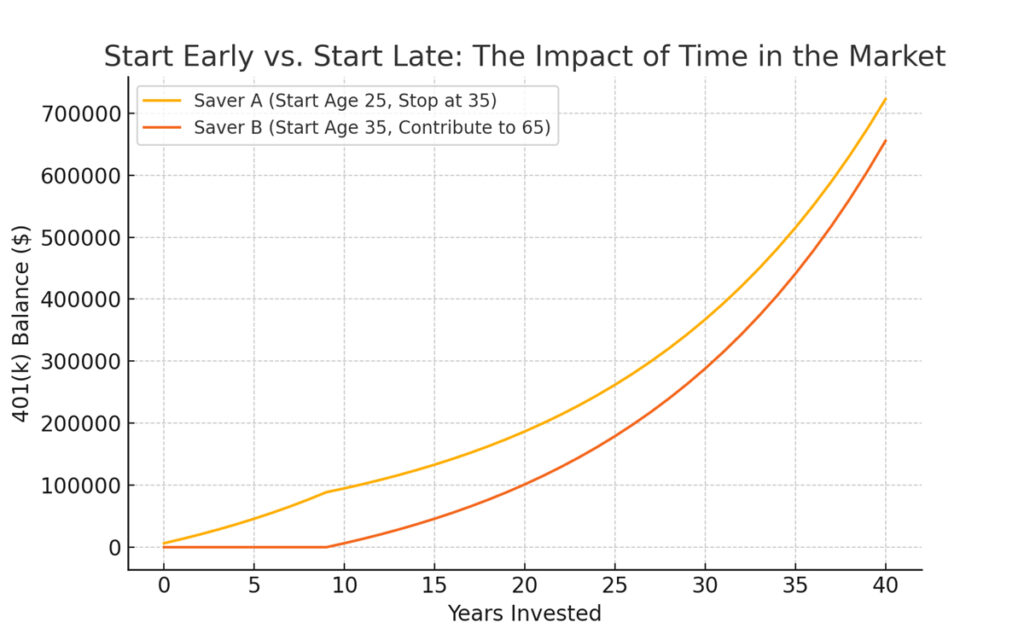

Here’s where it gets eye-opening. Suppose a 30-year-old saves $6,000 annually (about $500 monthly) at a conservative 6.5% annual return—realistic for a balanced portfolio. By 65, after 35 years, that’s roughly $744,000.

Now, delay until 40: Same $6,000 yearly for 25 years yields about $353,000. The difference? $391,000 gone, 52% of what you could have had. That’s the unbelievable math most 30-year-olds ignore.

Don’t believe me? Check similar calculations from Schwab, showing delays cost thousands. Time isn’t money, it’s multiplier.

Visualizing the 10-Year Retirement Delay Impact: A Comparison Table

To make this crystal clear, let’s compare scenarios. Assuming $6,000 annual contributions and 6.5% returns, here’s how starting ages affect your nest egg at 65.

| Starting Age | Years Saving | Total Contributions | Final Amount | % of Max Possible (from age 30) | Lost Opportunity |

|---|---|---|---|---|---|

| 30 | 35 | $210,000 | $744,208 | 100% | $0 |

| 35 | 30 | $180,000 | $505,000 | 68% | $239,208 |

| 40 | 25 | $150,000 | $353,326 | 48% | $390,882 |

| 45 | 20 | $120,000 | $237,000 | 32% | $507,208 |

| 50 | 15 | $90,000 | $148,000 | 20% | $596,208 |

(Data calculated using standard annuity formulas; inspired by Investopedia’s compound interest tools.) See the pattern? Each five-year delay chips away massively. For 30-year-olds, acting now maximizes that 100%.

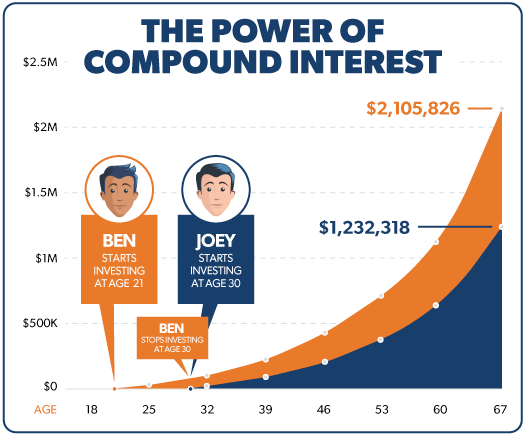

How Compound Interest Amplifies the 10-Year Retirement Delay Destruction

Compound interest is like a snowball rolling downhill, starts small, grows massive. But reverse it: Delay, and you miss the biggest rolls.

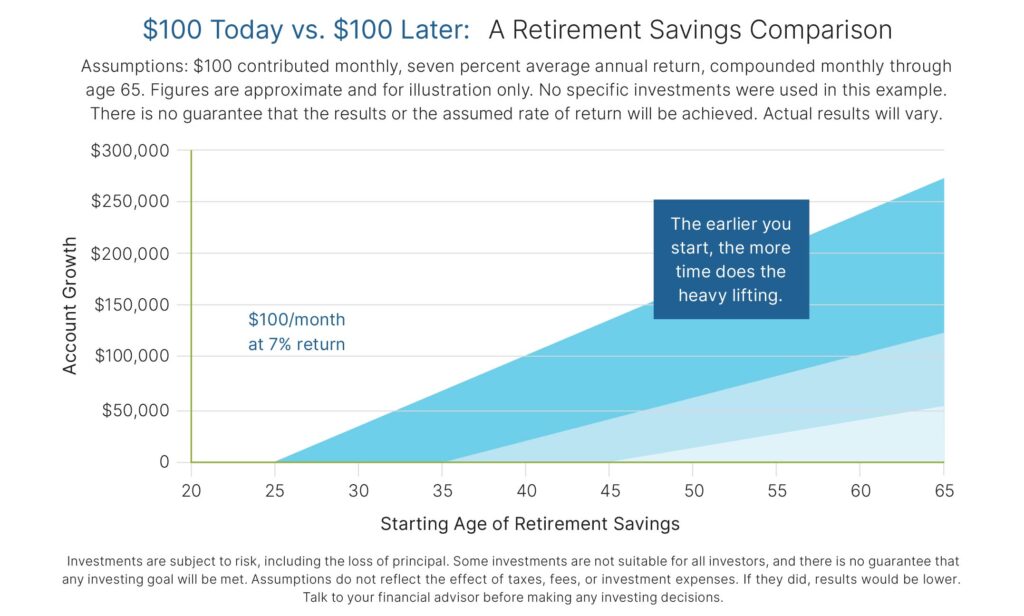

Take our example: That first decade from 30-40, your early contributions could grow 3-4 times by 65. Miss it, and you’re playing catch-up forever. Ramsey Solutions’ breakdown nails it: $100 monthly at 25 grows to $300k+ by 65 at 7%; wait till 35, it’s half.

In 2026, with volatile markets, steady compounding is your buffer. Ignore the math, and that 52% destruction becomes your reality.

Common Excuses 30-Year-Olds Use to Justify the 10-Year Retirement Delay

We’ve all been there. “I’m too young, retirement’s decades away.” Or “Student loans first.” Valid? Sure, but excuses compound too.

- “I can’t afford it now”: Even $50/month starts the habit. MassMutual’s 30s guide shows small starts beat zero.

- “Markets are risky”: Diversified funds average 6-8% long-term.

- “I’ll earn more later”: Raises often go to lifestyle, not savings. Delay math doesn’t care about future income.

- “Life’s for living”: Balance is key, save 10-15% without deprivation.

- “It’s too complicated”: Apps like Acorns simplify.

These mindsets lead to regret. Break them early.

Real-Life Stories: Victims of the 10-Year Retirement Delay Math

Meet Alex, a 55-year-old teacher who started saving at 40. “I thought 30s were for fun,” he says. Now, his fund’s $200k short, forcing part-time work post-65. Echoes Forbes’ late-starter tales.

Contrast with Sarah, who began at 30 with $200/month. By 50, compounding turned it to $150k+. “Unbelievable growth,” she shares on Reddit. Stories from r/personalfinance highlight: Early birds retire comfy.

The lesson? Math isn’t abstract, it’s your life.

Why 30-Year-Olds Are Prime Targets for the 10-Year Retirement Delay Trap

Your 30s: Peak energy, rising income, but mounting responsibilities. Loans, homes, families pull focus. Yet, this decade sets retirement trajectory.

Stats from Guardian Life: Save $5k/year at 30, hit $500k at 65 (5% return). Delay to 40? Double contributions needed.

In 2026, gig economy volatility amps risks. Don’t let distractions destroy 52% potential.

Steps to Avoid the 10-Year Retirement Delay and Master the Math

Ready to act? Here’s your roadmap.

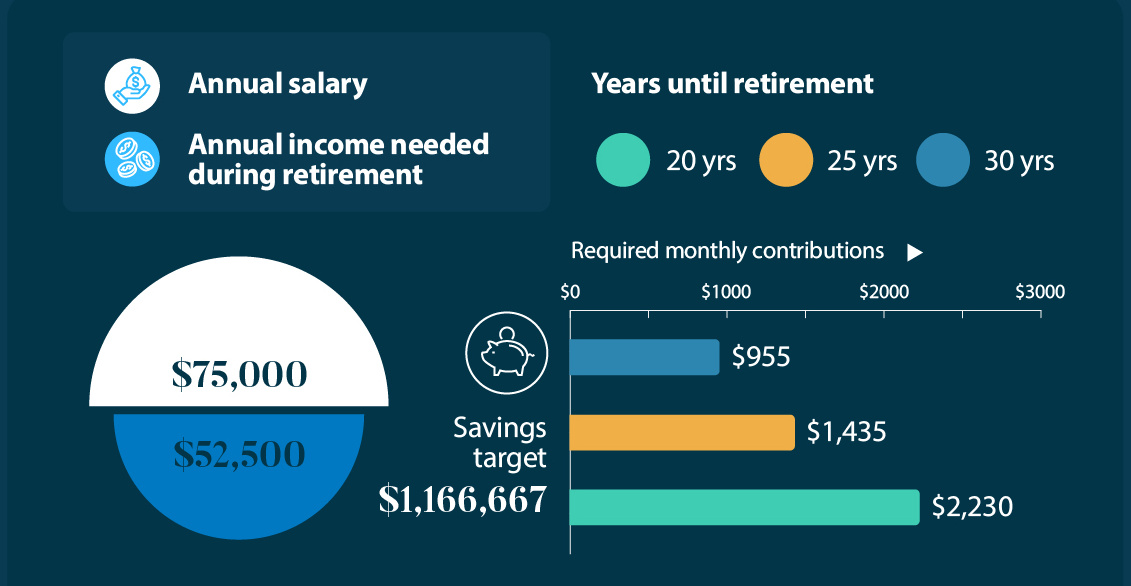

- Assess your current spot: Use Merrill Edge’s calculator to gauge needs.

- Start small, automate: Set 10% paycheck to 401(k)/IRA. Employer match? Free money.

- Max tax advantages: Roth IRAs for tax-free growth, per Principal’s tips.

- Diversify investments: Stocks for growth, bonds for stability.

- Cut unnecessary spends: Track with apps; redirect to savings.

- Boost income: Side hustles add $1k/year easily.

- Review annually: Adjust for life changes.

- Educate yourself: Read “The Simple Path to Wealth” for basics.

Consistency beats perfection. Start today.

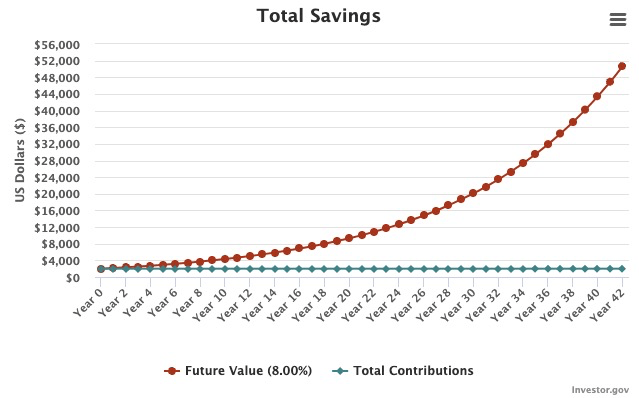

Tools and Calculators to Crunch Your Own 10-Year Retirement Delay Numbers

Don’t take my word—plug in yours. SmartAsset’s retirement calculator shows personalized delays.

Federated Hermes’ shortfall tool highlights gaps. Or FINRED’s compound savings calc for quick visuals.

These free resources make the unbelievable math tangible. Play around, see your 52% risk.

What If You’re Already Past 30? Reversing the 10-Year Retirement Delay Damage

Over 40? Not doomed. Catch-up rules allow extra contributions: $7,500 more in 401(k)s for 50+.

Work longer: A Wealth of Common Sense says delaying retirement from 62 to 70 halves needed savings.

Downsize lifestyle, invest aggressively (safely). Kotys Wealth advises 20-30% income to savings if late.

Hope isn’t lost, action is key.

The Broader Impact: How 10-Year Retirement Delay Affects Society in 2026

Zoom out: Millions delaying means strained Social Security, more elderly poverty. Brookings’ rule pushes 10% savings to cut risks.

For families, it means less inheritance, more burden. Educate kids early, break the cycle.

Overcoming Mental Barriers to Beat the 10-Year Retirement Delay

Fear math? It’s simple: Time > Amount. LinkedIn’s compound guide uses Rule of 72, double money every 11 years at 6.5%.

Mindset shift: Saving’s investing in freedom. Join communities for motivation.

Advanced Strategies: Maximizing Beyond the Basic 10-Year Retirement Delay Fix

Pro level: Tax-loss harvesting, HSAs for triple tax perks. Hancock Whitney’s 30s plan suggests blending.

Real estate? Rental income compounds too. Diversify wisely.

The Role of Inflation in Amplifying 10-Year Retirement Delay Risks

Inflation erodes purchasing power. At 3%, $1M today buys like $500k in 30 years. Delay worsens this, less time to outpace.

Voya’s cost of waiting projects milk at $7/gallon in 25 years. Save more, invest growth-oriented.

Inspiring Turnarounds: Beating the Odds After a 10-Year Retirement Delay

From Wiser Wealth: Late starter at 42 hits $632k by 67 with consistent $10k/year.

Reddit users share: Aggressive catch-up turned negatives to positives. You can too.

Final Thoughts: Don’t Let the 10-Year Retirement Delay Destroy Your Dreams

We’ve crunched the unbelievable math: A simple 10-year delay can obliterate 52% of your retirement through lost compounding. For 30-year-olds, this is your wake-up call, time’s ticking, but action flips the script.

Embrace the strategies, use the tools, and build that unbreakable nest egg. Your future self? Eternally grateful.

CTA: Crunch your numbers now with Schwab’s early savings calculator. Share this if it shocked you. What’s your savings start age? Comment below! Dive deeper into catch-up tips at Western & Southern. Share now!