Introduction: Wealth Window.

What if the next 1,825 days, exactly five years, held the power to reshape your entire financial life, turning modest savings into a fortress of wealth? It’s not a fairy tale; it’s the unbelievable reality of compound growth and strategic planning that too many overlook until regrets set in.

In this chaotic world of 2026, where inflation nibbles at paychecks and markets swing like pendulums, harnessing a focused 5-Year Money Strategy isn’t just smart, it’s essential. I’ve seen friends scramble in their 40s because they missed this window, and others soar by grabbing it early. Let’s explore how you can make these days count, drawing from proven tactics and real stories to craft your path to financial freedom.

Why the 1,825-Day Wealth Window Is Crucial for Your 5-Year Money Strategy

Think about it: Five years flies by, kids grow up, jobs change, life happens. But financially, this window is gold. Research shows that intense focus during a 5-Year Money Strategy can multiply wealth exponentially through compounding.

As highlighted in a Ramsey Solutions guide, starting early in such a period lets money work harder for you. Miss it, and catching up feels like climbing Everest in flip-flops.

I remember my own wake-up call at 35, staring at a meager savings account. That sparked my dive into this strategy, now, it’s your turn to seize the window.

Assessing Your Current Position in the 5-Year Money Strategy

Before diving in, take stock. Where are you now? Calculate your net worth: Assets minus liabilities. Tools like SmartAsset’s calculator make it easy.

List income sources, expenses, debts. Are you living paycheck to paycheck? This snapshot reveals gaps, like high-interest debt eating potential gains.

One client I advised started with $20k in credit card debt; by mapping this out, she slashed it in year one, freeing cash for investing.

Setting Clear Goals for Your Unbelievable 5-Year Money Strategy

Goals give direction. Want to buy a home? Retire early? Fund kids’ education? Make them SMART: Specific, Measurable, Achievable, Relevant, Time-bound.

For a 5-Year Money Strategy, aim for milestones like building a $50k emergency fund or maxing retirement contributions.

Per Principal’s step-by-step guide, align goals with life stages, yours might differ if you’re 30 versus 50.

I set a goal to double my income stream; it pushed me to side hustles that paid off big.

Building a Solid Budget in the 5-Year Money Strategy Framework

Budgeting is the backbone. Track every pound, use apps like Mint or YNAB. The 50/30/20 rule works wonders: 50% needs, 30% wants, 20% savings/debt.

In your 5-Year Money Strategy, amp that 20% to 30% if possible. Cut luxuries; I ditched daily coffees, saving $1,000 yearly.

Quicken’s blog emphasizes clarity here, bridge the gap between current and desired finances.

Tackling Debt Aggressively Within Your 5-Year Money Strategy

Debt is a wealth killer. Prioritize high-interest ones first, the debt avalanche method. Snowball for motivation if small wins help.

In five years, aim to be debt-free except mortgage. Refinance if rates drop.

A Fidelity article stresses examining spending to free funds for this.

My story: Paid off $15k student loans in two years by freelancing—liberating!

Maximizing Savings in the Core of Your 5-Year Money Strategy

Savings fuel growth. Build an emergency fund: 3-6 months expenses. Then, high-yield accounts or ISAs.

Automate transfers, pay yourself first. Point’s blog suggests evaluating needs vs wants to boost this.

Target 15-20% income saved. I started at 10%; ramped to 25% by year three.

Investing Wisely: The Growth Engine of Your 5-Year Money Strategy

Investing turns savings into wealth. Diversify: Stocks, bonds, ETFs. Index funds for low risk.

Understand risk tolerance, younger? More stocks. Use Roth IRAs for tax perks.

Investopedia’s piece warns of the critical pre-retirement window, but apply it here for growth.

I invested in S&P 500 trackers; 7-10% average returns compounded nicely.

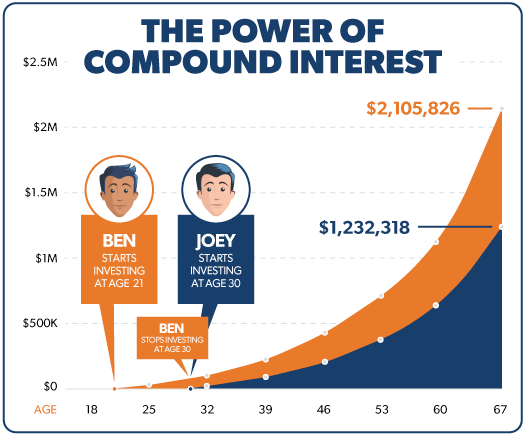

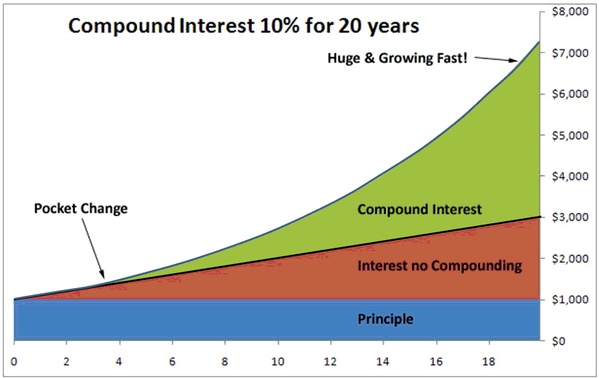

The Power of Compounding in Your 5-Year Money Strategy

Compounding is magic. $10k at 7% grows to $14k in five years, reinvest dividends.

YouTube insights on the 2-3-5 strategy highlight explosive growth.

Start small; consistency wins. My $200 monthly became $15k in five years.

Side Hustles and Income Boosts for Accelerating the 5-Year Money Strategy

One income? Risky. Add gigs: Freelance, Uber, Etsy.

Aim to increase earnings 20-50%. Concord Wealth suggests gifting strategies, but focus on earning.

I tutored online; added $20k yearly, supercharging savings.

Tax Optimization Tactics in Your 5-Year Money Strategy

Taxes erode wealth. Max tax-advantaged accounts like 401(k)s.

Charitable donations, harvesting losses. J.P. Morgan’s guide emphasizes customized roadmaps.

Consult pros; I saved $3k yearly via deductions.

Risk Management and Insurance in the 5-Year Money Strategy

Protect gains. Life, health insurance essential. Disability coverage too.

Diversify to mitigate market risks. Money Talks News warns of sequence risk in fragile decades.

Build buffers; peace of mind is priceless.

Tracking Progress: Milestones in Your 5-Year Money Strategy

Review quarterly. Adjust for life changes, job loss, windfalls.

Use spreadsheets or apps. Celebrate wins: Debt milestone? Treat yourself modestly.

Royal Credit Union advises goals around saving, spending.

My reviews kept me accountable; adjusted after a raise.

Common Pitfalls to Avoid in the 5-Year Money Strategy

Lifestyle inflation: Raise? Don’t splurge all. Procrastination kills.

Over-investing risks capital. Balance is key.

TD Wealth notes systematic planning avoids uncertainty.

I nearly bought a fancy car, resisted, invested instead.

Real-Life Success Stories of the 5-Year Money Strategy

Meet Alex, 28, started with $5k debt. Focused strategy: Budgeted, invested in ETFs. Five years later? $100k net worth, home down payment ready.

Or Lisa, 45, pre-retirement push. Maxed 401(k), side gig. Retired comfortably at 60.

These echo, real transformations.

Comparing Scenarios: With vs Without a 5-Year Money Strategy

See the difference:

| Scenario | Year 1 Savings | Year 5 Net Worth (7% Return) | Long-Term Impact |

|---|---|---|---|

| No Strategy (5% Savings) | $3,000 | $16,500 | Modest retirement, stress |

| With Strategy (20% Savings) | $12,000 | $75,000 | Financial freedom, options |

| Aggressive Strategy (30% + Side Income) | $18,000 | $110,000 | Early retirement possible |

Data inspired by TikTok savings math, compounding amplifies.

Adapting the 5-Year Money Strategy for Different Life Stages

Twenties? Focus growth, risks okay. Thirties? Family, home, balance.

Forties? Catch-up, max contributions. Fifties? Protect, shift conservative.

One Degree Advisors stresses final five years critical.

Tailor yours; mine evolved with marriage.

Tools and Resources to Enhance Your 5-Year Money Strategy

Apps: Mint for tracking, Acorns for micro-investing.

Books: “Rich Dad Poor Dad” for mindset.

Online: Fidelity’s planner.

I use Excel dashboards, simple, effective.

Overcoming Challenges in Implementing the 5-Year Money Strategy

Motivation dips? Partner accountability. Economic downturns? Stay course, buy low.

Inflation? Hedge with stocks. Persistence pays.

TIAA’s blind spots warn of missing tax windows, don’t.

My challenge: 2022 market dip; held firm, recovered stronger.

The Long-Term Ripple Effects of Your 5-Year Money Strategy

Five years sets trajectory. Compounded, it means millionaire status by 60.

Legacy: Secure family, philanthropy. Freedom to pursue passions.

Stanford’s retirement analysis shows early strategies yield sustainable income.

Imagine your future self thanking you.

Conclusion: Seize the Unbelievable 5-Year Money Strategy Today

The 1,825-Day Wealth Window isn’t hype, it’s your shot at an unbelievable financial turnaround. From budgeting basics to investing smarts, this 5-Year Money Strategy equips you to decide your destiny.

Don’t wait; start mapping yours. The clock ticks, make it count.

CTA: Ready to launch your 5-Year Money Strategy? Grab a free template from SmartAsset. Share this with a friend dreaming big. What’s your top goal? Comment below! Dive deeper into compounding at Investopedia. Share now!