Introduction: Steps to Retire in the Next 10 Years

What if you could wave goodbye to the daily grind in just 10 years, waking up to freedom instead of alarms? For many, early retirement feels like a distant fantasy reserved for the ultra-wealthy, but experts in the FIRE movement are finally spilling the secrets that make it achievable for everyday people.

As we close out 2025 and look to 2026, these 5 little-known steps to retire in the next 10 years are gaining traction among those tired of waiting until 65. Drawing from real strategies that have helped thousands quit early, let’s uncover what truly works.

Why Retiring in the Next 10 Years Is More Realistic Than Ever

The FIRE (Financial Independence, Retire Early) movement isn’t new, but in 2025-2026, it’s evolving with lower barriers thanks to high-yield accounts, remote work, and accessible investing tools. Traditional retirement at 65 assumes modest savings, but FIRE flips the script by prioritizing aggressive wealth-building now.

Experts note that with discipline, many in their 40s or 50s can hit financial independence sooner. As outlined in Investopedia’s FIRE guide, the key is a high savings rate and smart investing—often 50-70% of income.

But the little-known part? It’s not about earning millions; it’s about optimizing what you already have. Ignore these steps, and you’ll likely work longer than necessary.

Step 1: Calculate Your True FIRE Number, The Hidden Foundation for Retiring in 10 Years

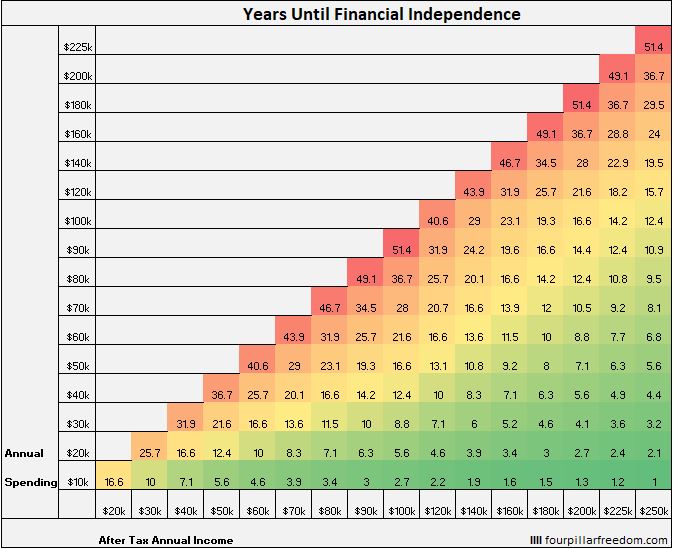

Most people guess how much they’ll need, but the shocking secret is precision. Use the 4% rule: Save 25 times your annual expenses (not income). If you need $50,000/year, aim for $1.25 million.

Little-known twist: Factor in variants like Coast FIRE (save enough early for compounding to finish the job) or Barista FIRE (part-time work for health insurance).

- Track current spending for 3 months.

- Subtract non-essentials to lower your number.

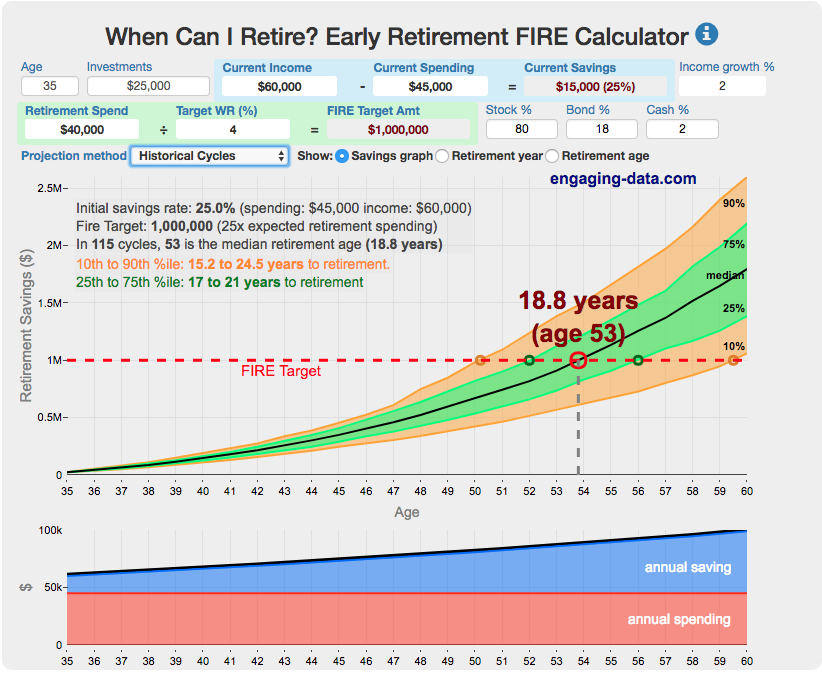

- Use free calculators like Engaging Data’s FIRE tool.

As NerdWallet explains, this step alone reveals if 10 years is feasible.

Step 2: Slash Expenses Ruthlessly, The Little-Known Power of Living Below Your Means

Experts agree: Cutting costs accelerates everything. Aim for a 50-70% savings rate to retire in 10 years or less, per the shockingly simple math.

Hidden insight: Focus on big wins, housing, transport, food not tiny lattes.

- Downsize home or geo-arbitrage to low-cost areas.

- Embrace minimalism for joy, not deprivation.

- Audit subscriptions and negotiate bills.

This step frees cash for investing, compounding your path to freedom. Many retirees say this mindset shift was transformative.

Step 3: Boost Income Strategically – Side Hustles That Fuel Early Retirement

Saving alone isn’t enough; experts recommend multiple streams. In 2026, remote gigs make this easier.

Little-known: Use skills for high-return hustles, not just extra hours.

- Freelance in your expertise (consulting, writing).

- Rental income or digital products for passive flow.

- Max employer matches first, free money!

As Bankrate suggests, incremental income supercharges savings without burnout.

Step 4: Invest Aggressively and Tax-Smart – The Compound Magic Experts Swear By

Once money is freed, invest it wisely. Broad index funds historically return 7-10%, turning consistent contributions into millions.

Under-the-radar: Prioritize tax-advantaged accounts.

- Max 401(k) ($23,500 in 2025, likely higher in 2026) and IRAs.

- Consider Roth conversions for tax-free growth.

- Bridge accounts for early access without penalties.

Per Vanguard’s insights, this step leverages compounding—the real “secret” to 10-year timelines.

Step 5: Plan for Healthcare and Risks – The Overlooked Step That Saves Retirements

Early retirement’s Achilles heel? Healthcare before Medicare (age 65). Experts finally emphasize bridging this gap.

Little-known options: HSAs for triple tax benefits, or Barista FIRE for employer coverage.

- Build a 6-12 month emergency fund.

- Diversify investments to weather volatility.

- Test your plan with “mini-retirements.”

As Ally highlights, ignoring risks derails more plans than low savings.

Savings Rate Impact: How It Shortens Your Path to Retire in 10 Years

Here’s a table showing years to retirement based on savings rate (assuming 5% real return, from Mr. Money Mustache and similar models):

| Savings Rate | Years to Retire (from scratch) | With Existing Savings Boost |

|---|---|---|

| 10% | 51 years | Slow traditional path |

| 30% | 28 years | Moderate acceleration |

| 50% | 17 years | Feasible for many |

| 60% | 12 years | Aggressive but doable |

| 70% | 8.5 years | Little-known fast track |

| 75% | <8 years | Expert-level commitment |

Higher rates = shorter timeline. Little-known: Even starting mid-career, 60%+ can hit 10 years.

Real Stories: People Who Retired in 10 Years Using These Steps

Take Vicki Robin, co-author of “Your Money or Your Life,” who inspired FIRE, many followers retired in under a decade by tracking every dollar.

Or modern examples from communities: A tech worker saved 70%, invested in indexes, and coasted to freedom at 45.

These aren’t outliers; they’re proof the steps work when applied consistently.

Adapting for 2026: Little-Known Tweaks for Today’s Economy

Inflation and markets fluctuate, but principles hold. In 2026, expect higher contribution limits and AI tools for tracking.

Hybrid approaches like Coast or Barista FIRE offer flexibility if full retirement feels daunting.

Conclusion: Your 10-Year Retirement Starts Today

These 5 little-known steps to retire in the next 10 years, precise calculation, ruthless cuts, income boosts, smart investing, and risk planning—aren’t flashy, but experts confirm they deliver results.

The excitement? Freedom on your terms, sooner than you think. In 2026, it’s more achievable than ever.

CTA: Run your numbers with a free FIRE calculator. Share this if you’re ready for change. What’s your biggest hurdle? Comment below! Dive deeper into variants at Mintos’ guide. Share now!